Commissioner scrambles to maintain insurers as nat-cats make state an increasing number of unattractive to carriers

Property

By

As some counties demand he declares a statewide state of emergency to forestall carriers from dropping policyholders, California’s Insurance coverage Commissioner Ricardo Lara has unveiled an effort to power insurers to renew writing insurance policies in high-fire-risk areas — a part of an general plan to deal with the state’s insurance coverage disaster.

It consists of three alternative ways insurers can meet minimal necessities for writing insurance policies in areas deemed “excessive danger” or “very excessive danger” by Cal Fireplace. Insurance coverage division regulators mentioned this hybrid method takes into consideration the state’s advanced geography in addition to the completely different danger ranges that massive and small insurers can afford to imagine. Lara mentioned this could assist householders who’ve misplaced protection or been pressured to show to the last-resort FAIR Plan.

Insurance coverage firms would have these three choices:

· Write 85% of their statewide market share in high-risk areas. The division explains it this fashion: “If an organization writes 20 out of 100 houses statewide, it should write 17 out of 100 houses in a distressed space.”

· Obtain one-time 5% development within the variety of insurance policies they write in high-risk areas.

· Broaden their variety of insurance policies 5% by taking individuals out of the strained FAIR Plan, a pool of insurers the state requires to offer fire-insurance insurance policies when property homeowners can’t receive insurance coverage elsewhere.

Insurers may meet these policy-writing quotas both on the county stage or the ZIP code stage.

Particularly, they might apply the 85% or 5% choice in counties regulators have recognized as distressed, or in ZIP codes regulators have deemed “undermarketed” and excessive danger — which means the ZIP codes have a minimum of 15% of insurance policies within the FAIR Plan and have a sure proportion of residents who can’t afford their premiums. Insurers who already meet the 85% threshold could be required to take care of that for a minimum of three years after a price software.

Or they’ll select the third choice, lowering insurance policies within the FAIR Plan statewide.

Regulators will replace these areas a minimum of yearly.

Gov. Gavin Newsom hailed Lara’s announcement as “crucial” to fixing the state’s insurance coverage disaster.

“Because the local weather disaster has quickly intensified, the insurance coverage system hasn’t been severely reformed in 30 years – that is a part of our technique to strengthen our market and get people the protection they want,” the governor mentioned in an announcement.

The assertion comes as San Bernardino County supervisors have requested Newsome to announce a state of emergency that may forestall insurers from dropping any extra policyholders.

“We’re attempting to get the Legislature, the chief department and the governor on board with the insurance coverage commissioner to direct regulatory change,” Supervisor Daybreak Rowe advised the San Bernadino Solar.

“San Bernardino has a variety of mountain and desert communities, and each communities are struggling to get householders’ insurance coverage,” she continued. “Shopping for a home and getting insurance coverage is rather more costly and tough in the event you reside in an space thought-about to have a better danger for fireplace and catastrophe.”

If Lara’s proposal works as supposed, householders may finally discover it simpler to purchase insurance coverage with enough protection, versus the costly fire-only insurance policies that many just lately have been pressured to purchase from the FAIR Plan.

The proposed choices aren’t technically necessities, as a result of the state can not legally require insurers to jot down both home-owner or business property insurance policies. However the state expects insurers to conform as a result of failure to take action would imply insurers wouldn’t be capable of benefit from one thing they’ve lobbied for lengthy and arduous: disaster modeling.

Lara unveiled the first part of his plan to allow for catastrophe modeling in March; that is the second a part of that plan. Disaster modeling takes into consideration historic knowledge and combines that with projected danger and losses — one thing insurers have been capable of do in each different US state however California. Insurers will be capable of use it there as soon as Lara’s general plan is lively – though the laws could not have impact till 2026 – commissioners need extra quick motion.

Lara’s newest announcement made clear what he needs from insurers to permit them to mannequin losses accurately – though the assertion is aimed on the public, in actuality the federal government is aware of that it’s dealing with an insurance coverage disaster.

“Insurance coverage firms must decide to writing extra insurance policies and my division might want to confirm these commitments and maintain them accountable,” Lara advised reporters on the finish of final week. Once they submit price evaluations, insurers will state which of the pathways they select. In the event that they don’t fulfill the necessities of that pathway, “my division will use its legislation enforcement authority and rethink price evaluations,” the commissioner mentioned. Meaning attainable decreasing of charges and even refunds, in response to his employees.

Lara’s employees mentioned they established the necessities for minimal protection in distressed areas after speaking with completely different stakeholders, together with insurance coverage firms that mentioned the necessities have been achievable. However the draft laws additionally embody a attainable out for insurers, who would be capable of request “various commitments” due to adjustments of their dimension or scope of protection, or the “frequency or severity of current occasions” affecting them.

“The remainder of the plan will nonetheless imply fast, huge price hikes,” she advised CalMatters. The group, nevertheless, has been accused of inflicting the very insurance coverage disaster that’s gripping the state now by getting California Proposition 103 narrowly handed in 1988 with Ralph Nader’s assist.

The laws required insurers to get the Insurance coverage Commissioner’s approval earlier than implementing insurance coverage charges – The Worldwide Heart for Legislation and Economics has calculated that prop.103 has price Californians $25 billion – regardless of Client Watchdog’s claims on the contrary.

The laws required insurers to get the Insurance coverage Commissioner’s approval earlier than implementing insurance coverage charges – The Worldwide Heart for Legislation and Economics has calculated that prop.103 has price Californians $25 billion – regardless of Client Watchdog’s claims on the contrary.

One insurance coverage trade group, the American Property Casualty Insurance coverage Affiliation, didn’t handle any specifics of the plan launched as we speak, aside from to say it “stays dedicated” to working with the Insurance coverage Division.

Rex Frazier, president of the Private Insurance coverage Federation of California, known as the proposal “advanced, with many trade-offs,” however mentioned his group additionally stays dedicated to working with Lara.

Lara has but to launch the opposite principal components of his general plan, together with improving the FAIR plan and permitting insurers to incorporate reinsurance prices of their premiums.

The place does Lara need extra insurance coverage?

The Division of Insurance coverage has launched a listing of ‘distressed counties’ that it requires insurers to decide to writing extra insurance policies for:

|

County

|

Inhabitants

|

|

Tuolumne

|

54,531

|

|

Trinity

|

14,768

|

|

Nevada

|

104,666

|

|

Mariposa

|

17,300

|

|

Plumas

|

19,639

|

|

Alpine

|

1,204

|

|

Calaveras

|

44,708

|

|

Sierra

|

3,226

|

|

Amador

|

39,637

|

|

El Dorado

|

191,385

|

|

Mono

|

13,796

|

|

Lake

|

65,417

|

|

Mendocino

|

85,934

|

|

Siskiyou

|

43,530

|

|

Butte

|

220,200

|

|

Lassen

|

30,999

|

|

Shasta

|

182,029

|

|

Tehama

|

66,219

|

|

Santa Cruz

|

268,712

|

|

Humboldt

|

136,779

|

|

Napa

|

137,744

|

|

Del Norte

|

27,860

|

|

Modoc

|

8,910

|

|

Placer

|

425,166

|

|

Monterey

|

439,035

|

|

Marin

|

264,353

|

|

San Luis Obispo

|

284,010

|

|

Ventura

|

847,504

|

Key statistics & knowledge on the California FAIR Plan

Overview

The California FAIR Plan Affiliation (FAIR Plan) is the Golden State’s security internet, providing property insurance coverage to customers who can’t safe protection via customary insurance coverage suppliers. It was launched in 1968 following bushfires and the state’s riots.

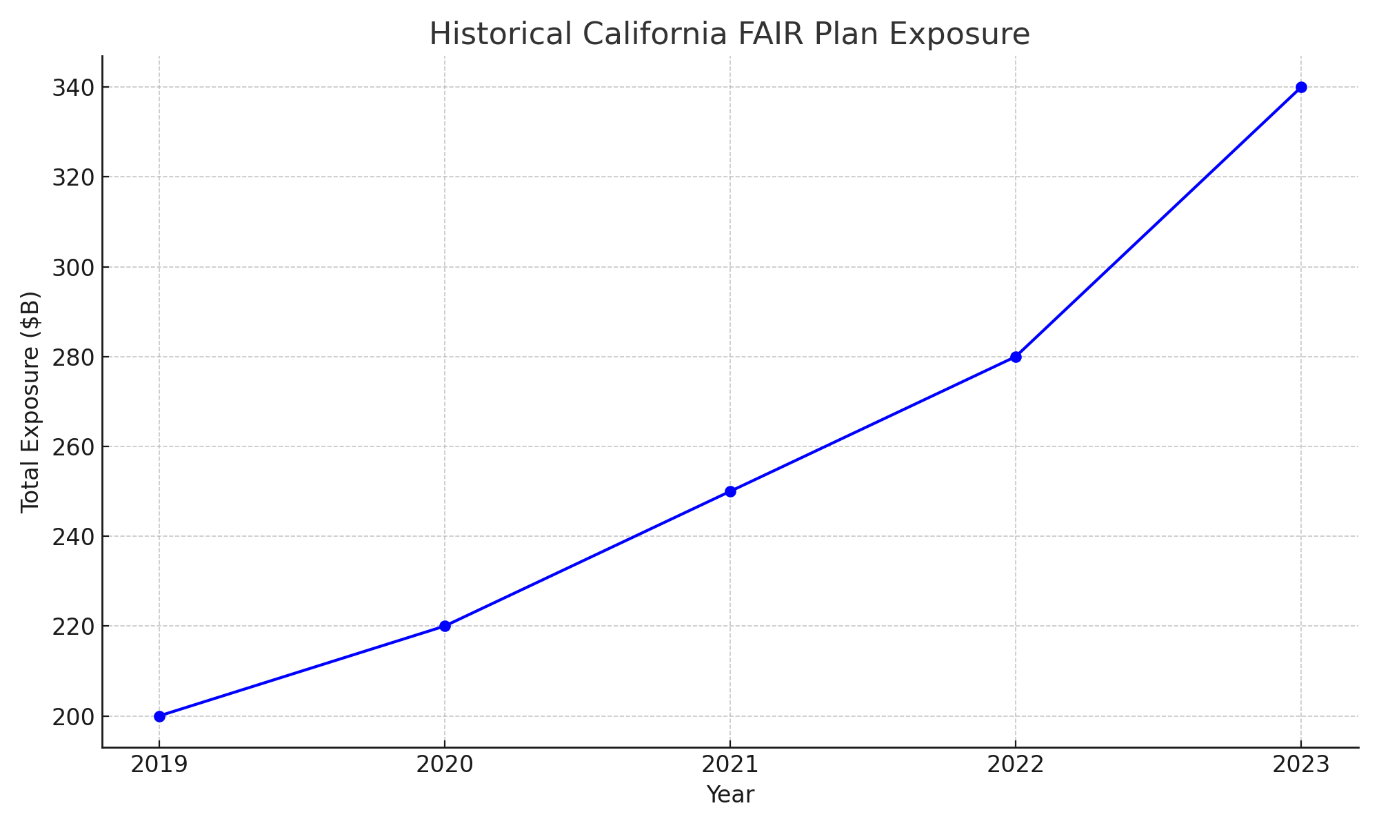

As of March 2024, the whole publicity of the FAIR Plan has reached $340 billion. This marks a notable 20% enhance from the earlier yr, highlighting the rising dependence on this insurance coverage choice which the President of the Private Insurance coverage Federation of California, Rex Frazier has known as a “Home of playing cards.”

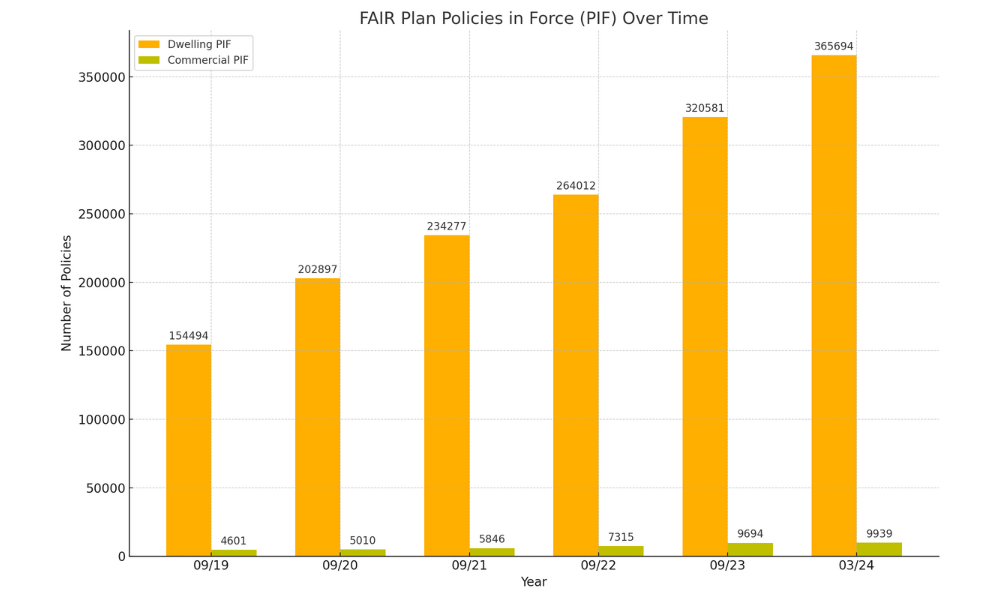

And regardless that the state authorities is eager to attempt to offload the danger of this state sponsored backstop, the issuance of insurance policies by the FAIR Plan has skilled substantial development in recent times:

- 2023: A complete of 89,995 new insurance policies have been issued, reflecting a robust demand for FAIR Plan protection.

- First two quarters of 2024: Already, 73,839 insurance policies have been issued, indicating that this upward development is constant.

Development by coverage sort

- Dwelling insurance policies: There was a 137% enhance within the issuance of dwelling insurance policies since 2019.

- Industrial insurance policies: The issuance of economic insurance policies has elevated by 116% throughout the identical interval.

Geographic protection

The FAIR Plan offers protection throughout numerous geographical areas, making certain that property insurance coverage is accessible to people in city, suburban, and rural areas, together with these in high-risk zones.

Projections point out continued development in each complete publicity and the variety of insurance policies issued by the FAIR Plan, given the rising frequency and severity of pure disasters, coupled with shifts within the conventional insurance coverage market.

Associated Tales

Sustain with the most recent information and occasions

Be part of our mailing checklist, it’s free!

{kind=link}