As its title implies, dividend paying complete life insurance coverage is a type of complete life insurance coverage that earns a dividend. The official insurance coverage time period used to determine a dividend paying complete life coverage is “collaborating” as a result of the coverage participates within the divisible surplus (i.e. income) of the insurance coverage firm.

The choice to a dividend paying complete life coverage is a non-dividend paying (additionally known as non-participating or non-par) complete life insurance policies. As soon as a non-dividend paying complete life coverage is issued, it would by no means earn a dividend no matter how worthwhile the insurance coverage firm is. A dividend-paying complete life coverage, then again, is eligible to dividends, however this doesn’t all the time means it would earn dividends.

Life insurance coverage dividends present a number of worth that improve numerous options of an entire life coverage past the assured options. Life insurance coverage dividends additionally take pleasure in a number of tax favorable advantages.

How do Entire Life Dividends Work?

Annually the life insurance coverage firm’s board of administrators appears at firm income and decides how a lot of those income to pay to policyholders who personal dividend-paying insurance policies. As soon as declared, the policyholder will earn the dividend on the subsequent coverage anniversary. The dividend earned will go in the direction of no matter dividend option the coverage proprietor at present chosen.

It is necessary to grasp that whereas the dividend cost can develop over time, the forces that have an effect on a rising dividend differ. This implies the precise dividend cost could also be roughly than the earlier 12 months’s dividend cost. I deliver this up as a result of most life insurance coverage ledgers historically assume a situation the place dividend funds constantly enhance. Whereas that is attainable, it is not often the way in which issues works out in actual life.

How do Dividends Have an effect on A Entire Life Coverage’s Money Worth?

Dividends can improve a complete life coverage’s money worth by means of the paid-up additions dividend possibility. This feature makes use of the dividend to buy further mini complete life insurance policies which might be instantly paid-up and have instant money worth. These insurance policies connect to your complete life coverage and their demise profit and money worth provides to your complete life coverage’s demise profit and money worth.

Moreover, these paid-up additions can earn dividends so you’re successfully compounding the expansion of your complete life coverage with this selection. The Dividend purchases paid-up additions, which can earn extra dividends. These further dividends will buy much more paid-up additions, which in flip will go in the direction of the acquisition of much more paid-up additions.

How do Dividends Have an effect on A Entire Life Coverage’s Loss of life Profit?

Dividends can have an effect on the demise profit of an entire life coverage in two methods.

First, using paid-up additions can even enhance demise profit. For each $1 that goes in the direction of a paid-up additions, you’ll obtain some a number of of demise profit (e.g. $1 used in the direction of paid-up additions would possibly create $3 in demise profit). The precise quantity varies relying on the age of the insured of the coverage. As we already coated, paid-up additions will compound as a result of they themselves earn dividends sooner or later. This can trigger your total complete life demise profit to develop exponentially as time goes on.

Second, most complete life insurance policies have a dividend choice to buy time period life insurance coverage. This makes use of the dividend cost to buy time period life insurance coverage that provides to the gross demise good thing about your complete life coverage. This can actually increase how a lot demise profit you obtain along with your coverage. As a result of it’s time period insurance coverage, it’s best to perceive that his demise profit just isn’t everlasting. You must also perceive that you’d select this selection alternatively to paid-up additions, so you will have to weigh which one provides you extra of what you’re searching for each now and sooner or later. This dividend possibility will do nothing for accumulating money worth in your complete life coverage.

What Causes the Dividend Cost to Go Up?

There are two variable behind an growing dividend cost over time. As soon as variable the policyholder can management. That is using the paid-up additions dividend possibility, or making elective paid-up addition funds by means of a selected rider.

The opposite variable is the profitability of the insurance coverage firm. If the insurance coverage firm turns into extra worthwhile year-over-year, there’s a good probability the corporate will enhance the dividend payable to policyholders. It is value noting that the majority dividend-paying complete life insurance policies come from mutual life insurance coverage firms. A lot of these insurance coverage firm place possession within the firm within the palms of the policyholders, so these firms work completely for the good thing about policyholders. Given this construction, it is smart {that a} extra worthwhile mutual life insurance coverage firm is eager to pay extra dividends to its policyholders.

What Causes the Dividend Cost to Go Down?

Once more, the forces that trigger a dividend to say no are partly as much as the coverage proprietor and partly as much as the life insurance coverage firm. Examples that trigger a dividend to go down embrace: the coverage homeowners withdrawal of sure money values from the coverage, the set off of a reduce paid-up nonforfeiture benefit, and the life insurer’s decline in profitability from one 12 months to the subsequent.

Are you able to Withdraw Dividends from a Entire Life Coverage?

Sure you possibly can withdraw dividends from a complete life coverage. There are two major methods you go about doing this.

First, you should utilize the dividend option to obtain the dividend cost in money. This can end in a direct cost of the dividend to you every year. The insurance coverage firm can pay you regardless of the calculated dividend payable in your complete life coverage is as a money dividend despatched as a examine across the time of your coverage anniversary.

The second possibility in case you are utilizing the paid-up additions dividend option, is to request a withdrawal from the coverage (some firms will particularly name this a withdrawal of dividend additions). This leads to a give up of the paid-up additions bought with dividends. This can end in a discount of the general demise profit on the coverage (demise profit created by the paid-up additions you’re withdrawing). You’ll then obtain a examine within the quantity of the money worth of the paid-up additions you requested to withdraw.

Are Entire Life Dividends Taxable?

Entire life dividends have a number of tax favorable options that make the cost of dividends largely non-taxable to you. Basically, dividend are not taxable, however there are just a few circumstances that would make them taxable.

First, in case you are taking the dividend as a money cost it’s often a non-taxable cost. There are circumstances that would develop over time that might change this. The precise circumstances is a cost of dividends that exceeds your coverage price foundation.

For instance, assume that you simply personal a complete life coverage into which you paid a complete of $50,000 in premiums. You opted to obtain the dividend as a money cost and starting this 12 months, the overall dividends paid to you from inception of the coverage equals $55,000. You’ll owe taxes on $5,000 in dividends and can now owe taxes on all future dividends acquired when you pay no additional premiums into the coverage.

Second, when you choose to withdraw money out of your coverage and also you withdraw a sum in extra of the premiums you paid into the coverage, you’ll owe taxes on the quantity withdrawn above the sum of the premiums you paid.

For instance assume the identical situation above the place you’ve gotten a complete life coverage into which you paid $50,000 in premiums. Let’s additionally assume that you’ve got $110,000 in money worth on this coverage. Additionally assume on this situation that you simply used the dividend choice to buy paid-up additions in all years. You select to withdraw $65,000 from the coverage. You’ll owe taxes on $15,000 of this withdrawal as a result of that’s the distinction between what you paid in premiums and what you faraway from the coverage. Additionally any subsequent withdrawals shall be taxable until you proceed to make premium funds.

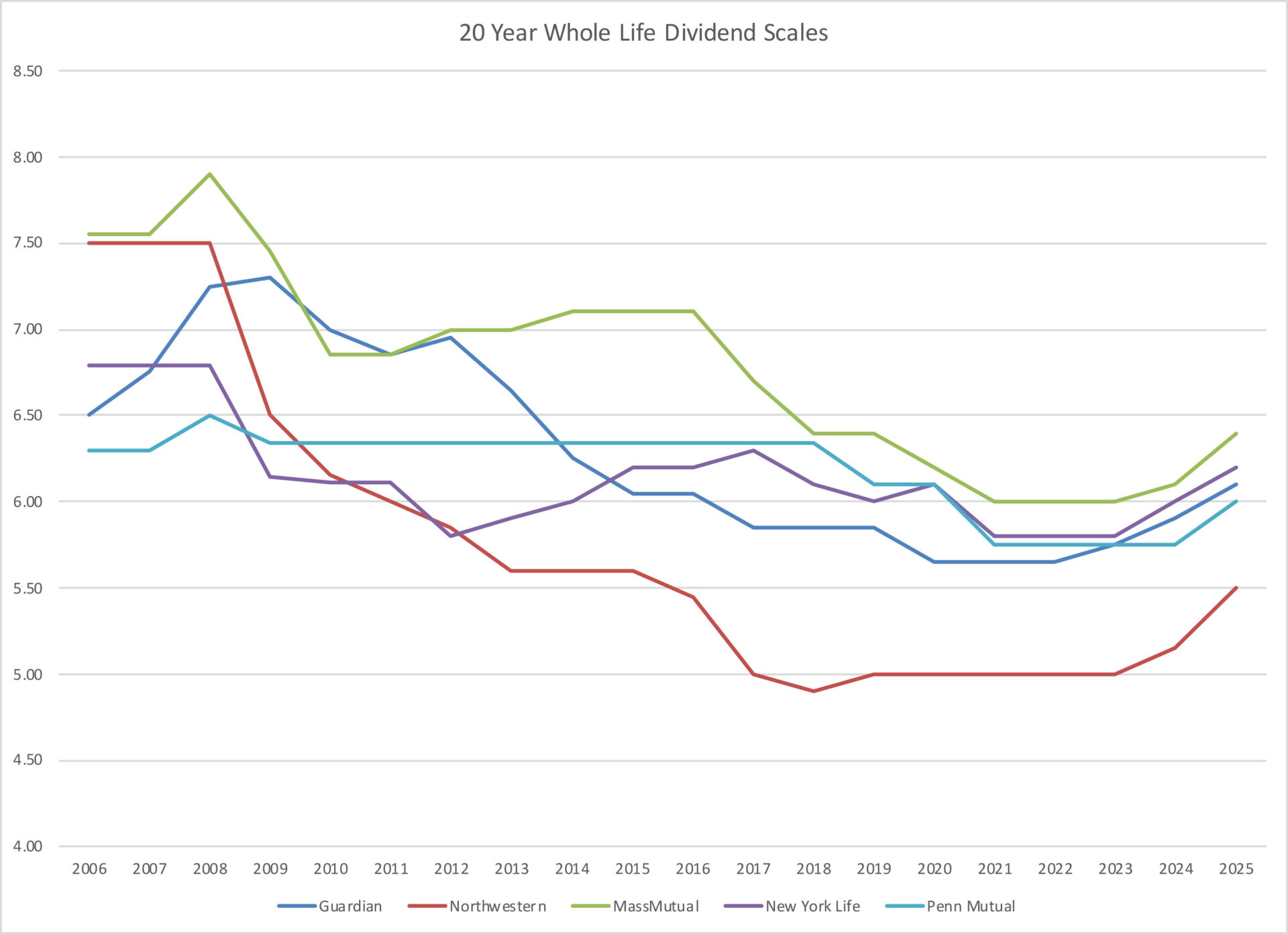

Historic Entire Life Dividend Chart

Entire life dividends can and do change over time. Here is a chart that maps out modifications amongst numerous complete life firms over the previous 20 years:

Two main observations from this chart are 1.) complete life dividend charges have a tendency to stay shut throughout firms and a pair of.) some firms modified their dividend price much more considerably over this time interval than others. Remember that the dividend price just isn’t a unified metric and one firm’s price just isn’t immediately comparable to a different. We are able to acquire some perception from wanting on the price of change at one firm to match to a different, however we can not evaluate absolutely the dividend price worth amongst life insurance coverage firms.

The general development is a decline adopted by a reversal unfolding given present financial situations. Life insurers realized substantial will increase in funding profitability as rates of interest rose following the COVID Pandemic.

{kind=link}

wl1uxl