The paid up additions characteristic of an entire life insurance coverage coverage is likely one of the strongest elements with respect to money worth accumulation. Most complete life merchandise have a paid up additions (PUA) characteristic, however they will all work a little bit in another way so it is vital to notice that one firm’s strategy may fluctuate considerably from others.

However earlier than we clarify how they work…

What Are Paid Up Additions?

Paid up additions can be found via a rider that’s added to an entire life insurance coverage coverage. The PUA rider permits the coverage proprietor to buy extra paid-up insurance coverage on their coverage. That every one sounds very technical, so let’s discover what that truly means for you in case you’re taking a look at money worth life insurance coverage (complete life specifically) and making an attempt to determine if it is the proper match.

The PUA rider is the mechanism used to put extra cash right into a taking part complete life insurance coverage coverage to extend coverage money worth efficiency. Each greenback of premium that’s allotted to the paid up additions rider creates a small paid up insurance coverage coverage that has its very personal money worth that’s created instantly. Typically, complete life insurance coverage insurance policies which have a considerable portion of the full premium allotted to paid up additions will outperform these that don’t make the most of PUAs.

There are additionally numerous paid-up additions choices out there from every insurance coverage firm. It could all appear difficult however cling in there, we’re gonna clarify it in a number of methods and supply examples as an example the way it works. We need to assist everybody perceive paid-up additions and their utility to life insurance coverage insurance policies.

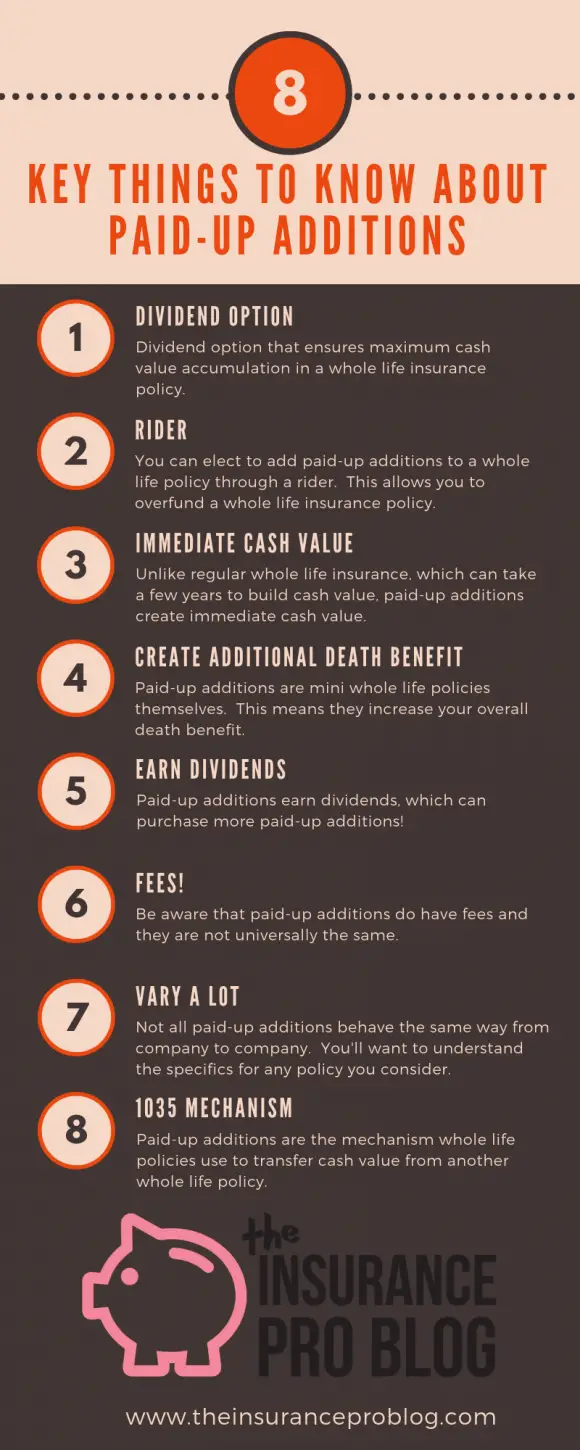

8 Issues to Perceive About Paid Up Additions

It makes excellent sense to dedicate a while to the dialogue of paid-up additions and their function in money worth life insurance coverage. You’ll discover them below a number of completely different names (extra insurance coverage rider, enricher rider, enhanced paid-up additions, and so on.), however it all means the identical factor.

The vital factor to grasp is PUAs and the PUA rider are essential for making a cash-rich coverage. At present we’ll enable you to perceive how they perform inside a well-designed coverage that helps you obtain your aim of specializing in most money worth build-up.

With almost 20 years of working within the life insurance coverage trade and having offered lots of of complete life insurance coverage insurance policies over the timeframe, we’ve precise, real-world expertise with all of this. Actually, the Insurance coverage Professional Weblog itself is the longest repeatedly working monetary weblog dedicated to data on life insurance coverage.

So once we sat down to determine how finest to clarify PUAs, we got here up with 8 key features you have to perceive to squeeze probably the most worth from them

The 8 key issues are:

- It’s a Dividend Option

- It’s also a Rider

- PUAs have Immediate Cash Value

- They have their own Death Benefit

- They Earn Dividends

- Have their own Load Fees

- Can Vary a lot from Company to Company

- PUAs are the Mechanism used for 1035 Exchanges for Whole Life Insurance

Utilizing the Dividend Choice to Buy PUAs

Quite a lot of complete life insurance coverage policyholders have expertise with paid-up additions however most could not notice this. Probably the most widespread dividend options used for complete life insurance policies is the choice to buy paid-up additions. This implies the insurance coverage firm takes the dividend earned on a whole life coverage and makes use of these funds to buy the additions for the policyholders.

For these searching for the quickest accumulation of complete life insurance coverage money values, there is no such thing as a higher possibility than buying paid up additions. I will clarify later on this weblog publish why that’s.

For many insurers, the dividend choice to buy paid up additions is the default possibility. So if the policyholder or agent don’t elect a distinct possibility, the life insurer will mechanically assume this feature

The PUA Rider

Along with being a dividend possibility, paid up additions can be a rider. This implies the policyholder can select so as to add the PUA characteristic to his/her coverage and elect to make a fee to the coverage solely for the aim of shopping for PUAs.

This differs from the dividend choice to buy PUA’s as a result of now the policyholder is selecting to take exterior funds and use them t0 buy the additions. This cash doesn’t characterize a dividend earned on the entire life coverage.

To be clear, many complete life insurance coverage insurance policies afford the power to each use the PUA dividend possibility and elect the rider thus permitting the policyholder to each buy PUAs with their dividends and purchase paid up additions instantly with extra funds they determine to contribute to the coverage.

Have Rapid Money Worth

When somebody who owns complete life insurance coverage chooses to purchase paid up additions along with paying their base complete life insurance coverage premium, they acquire a right away benefit–the paid up additions produce rapid money worth. This money worth features equally to the remainder of the money worth within the coverage. The policyholder can pledge this money worth for a coverage mortgage. Moreover, the policyholder can give up the paid-up addition and obtain its money worth–we generally consult with that is “withdrawing” cash from an entire life coverage.

A greenback used to buy a paid-up addition, creates a greenback of money worth (minus any charges related to the paid-up additions, see the charges part beneath). This creates a lot sooner money worth in the entire life coverage versus normal base complete life insurance coverage premium, which may take years to create money worth for the policyholder.

Creates Rapid Demise Profit

Paid-up additions additionally create a right away demise profit, and this demise profit is a a number of of the {dollars} used to buy the paid-up addition. For instance, a greenback used to buy a paid-up addition would possibly create 5 {dollars} in demise profit.

This demise profit is instantly “paid up” (therefore the identify) and requires no additional funds to stay in drive. Paid up additions might be considered miniature paid-up complete life insurance policies connected to a bigger complete life insurance coverage coverage. This implies the PUA characteristic (whether or not or not it’s via the dividend possibility or an elective rider) augments the full general demise profit of an entire life insurance coverage coverage. Over a number of years, the PUA characteristic may create a bigger demise profit than initially bought on the entire life coverage.

The quantity of demise profit acquired via every paid-up additions buy will depend on the age of the insured. Because the insured below the coverage ages, the a number of of demise profit created per greenback used to buy the PUAs declines.

For instance, a 30-year-old would possibly obtain $8 in demise profit for each $1 used to buy a paid-up addition whereas a 50-year-old would possibly obtain $3 in demise profit for each $1 used to buy a paid-up addition.

Earns Dividends

I discussed earlier that paid up additions might be considered miniature paid-up complete life insurance policies. These miniature insurance policies are taking part insurance policies, which merely signifies that they too earn dividends.

The importance of this reality is delicate however substantial. As a result of PUAs earn dividends, there’s a compounding impact that is created by the continuous buy of PUAs. Extra bought, means extra dividends earned. When dividends themselves go in the direction of the acquisition of extra PUAs, this creates extra PUAs which in flip buy extra paid-up additions, which earn extra dividends, which buy extra paid-up additions, and and so on.

There actually is not any higher option to develop money worth rapidly in with an entire life insurance coverage coverage than via the usage of paid up additions. It virtually looks as if magic.

Load Charges

PUAs often have a one time payment assessed at buy. Insurance coverage corporations categorical these charges as a proportion of the acquisition quantity identical to a load payment assessed in opposition to a mutual fund.

For instance, if the paid-up additions load payment is 10% and a policyholder makes use of $1,000 to buy paid-up additions, then the payment is $100. The $100 goes to the insurance coverage firm and the policyholder has $900 in rapid money worth created by the paid-up additions. There are not any extra ongoing charges for paid-up additions.

Charges can (and often do) differ relying on the best way policyholders buy paid-up additions. The instance above most carefully depicts how charges work for paid-up additions bought via a rider.

The fee charged by insurance companies varies quite a bit amongst insurers. It is tempting to check paid-up additions by load charges and counsel that decrease is healthier. Nonetheless as a result of most complete life merchandise are issued by insurers with a direct curiosity in returning income to policyholders, a better paid-up additions payment would not at all times imply a lower-performing coverage.

Variation Throughout Insurers is sort of Limitless

The precise performance of the paid-up additions rider varies significantly from one insurer to the following. Whereas most behave fairly straightforwardly regarding the dividend choice to buy paid-up additions, the paid-up additions rider differs significantly amongst life insurance coverage corporations.

Insurers even have a follow of calling the paid-up additions rider various things. Some widespread names are: extra premium rider, extra paid-up insurance coverage rider, elective everlasting safety, enricher rider, and supplemental insurance coverage rider. All of them imply and, for probably the most half, do the identical factor.

Some insurers differentiate between a lump sum and scheduled paid-up additions rider. The distinction being the previous permits a single fee across the outset of the coverage whereas the latter permits ongoing funds a number of years into the longer term.

Sure insurers allow a big degree of flexibility within the precise fee of the paid-up additions rider whereas others require a certain quantity be paid annually.

Most insurers impose yearly and/or lifetime limits on the sum of money a policyholder can place into the paid-up additions rider. This restrict may be a set quantity or a a number of of some foundation akin to the quantity of base complete life premium on the coverage. Insurers place these limits as a result of they fear concerning the legal responsibility created by the ever-increasing demise profit caused by paid-up additions.

The Mechanism for a 1035 Alternate

For these searching for to utilize the tax-free 1035 transfer of cash values from one life insurance coverage to an entire life insurance coverage coverage, paid-up additions are a required characteristic of the brand new complete life product. The paid-up additions rider is the mechanism via which the money switch can stream into the brand new complete life coverage. With no paid-up additions rider, the brand new complete life coverage can not settle for the funds.

The excellent news is, virtually all complete life insurance policies issued in america have a minimum of a paid-up additions characteristic in place to simply accept 1035 alternate cash.

The “Supercharger” Rider

There have been books written about complete life insurance coverage and utilizing your complete life coverage as a private banking system. These books typically make reference to a rider that supercharges the buildup of money values in an entire life insurance coverage coverage. All of these references are referring to the paid-up additions rider.

The paid-up additions rider is most frequently used purely as a strategic option to improve the money worth of an entire life insurance coverage coverage. Whereas paid-up additions do create extra demise profit, it is uncommon to return throughout a circumstance the place one makes use of them purely to extend the demise profit.

Whether or not a life insurance coverage coverage design merely provides a PUA rider on prime of an entire life premium or makes use of time period life mixing to open up extra funding capability, the paid-up additions rider is a should for these searching for cash-rich complete life insurance policies.

{kind=link}