Podcast: Play in new window | Download

Entire life insurance coverage can play an essential position in your retirement income planning. This assertion may go towards the grain of recommendation you see supplied by funding salespeople, however I feel we have displayed ample examples over the previous decade that entire life insurance coverage not solely works as a retirement earnings instrument, but it surely accomplishes the duty terribly effectively.

However there’s one thing else we have not spent a lot time telling you about. One thing “baked in” to entire life insurance coverage that places it in a robust place to take care of rising prices in retirement.

How Do Folks Generate Revenue with Entire Life Insurance coverage?

Maybe you’ve got seen a complete life insurance coverage proposal–we regularly name them “illustrations“–and on this proposal, you noticed a static earnings determine spanning a interval like your mid 60’s to your mid 80’s. You might need thought, “hey, that is cool. I can retire after which obtain X quantity of {dollars} yearly from this life insurance coverage coverage.”

However the fact is folks hardly ever ever do this.

Usually, retirees use their property to generate the earnings they want–and that is it.

Entire life insurance coverage is not any totally different on this respect. So whereas a coverage may be able to producing a certain quantity of earnings, most individuals have a tendency to make use of some quantity lower than that.

And taking much less cash from a complete life coverage comes with an additional benefit for later in life. Let’s take a look at an instance.

Entire Life Revenue Instance

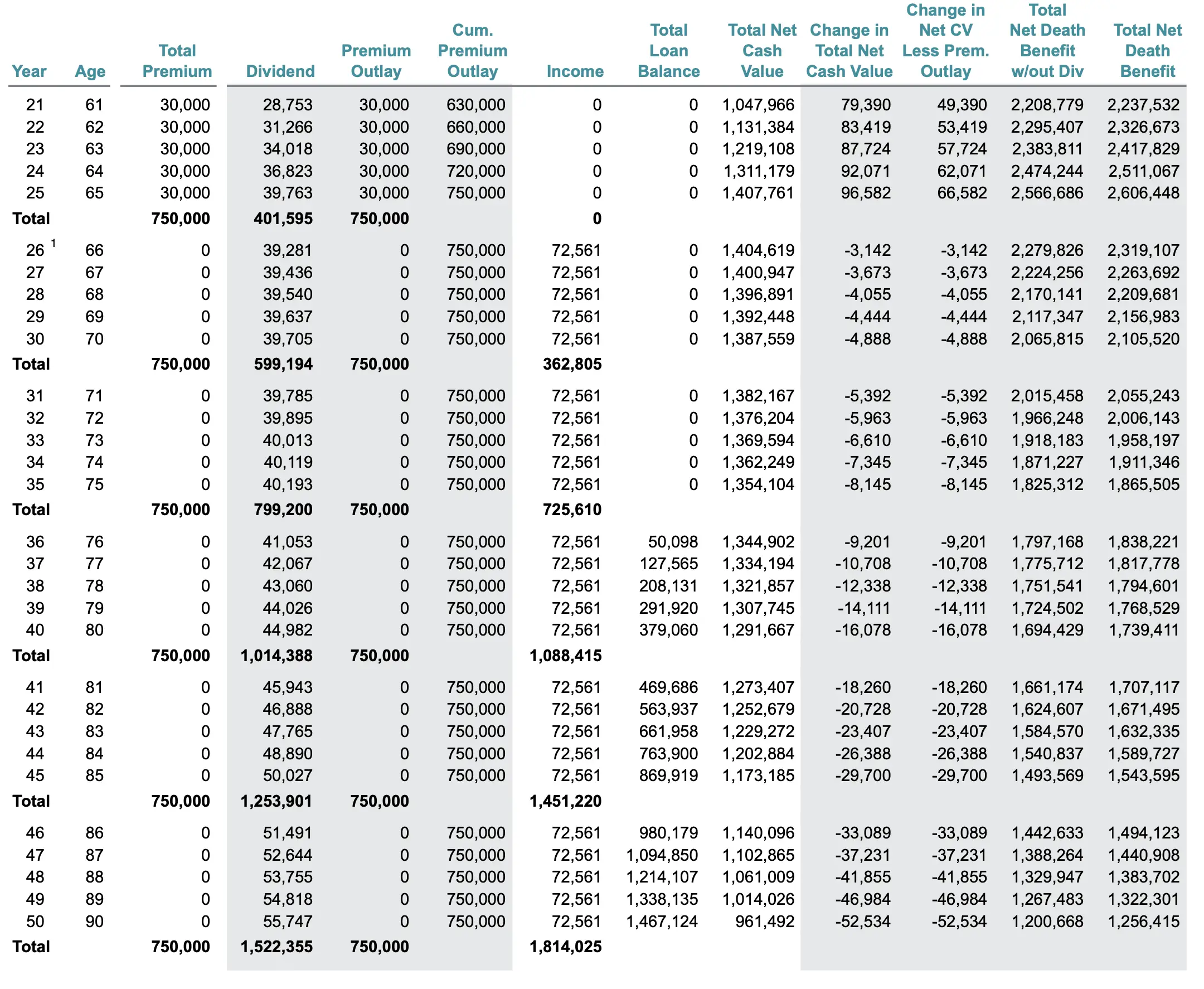

This ledger exhibits the earnings outcomes for a 40-year-old male who purchases a complete life coverage and contributes $30,000 per yr to the coverage by way of his age 65. At age 66, he begins utilizing the entire life coverage for retirement earnings. This ledger exhibits us the utmost earnings obtainable to him from age 66 to age 100–the ledger above is a snippet from the complete ledger.

As you may see, he can produce as much as $72,561 per yr together with his entire life insurance coverage coverage, which is not dangerous in any respect.

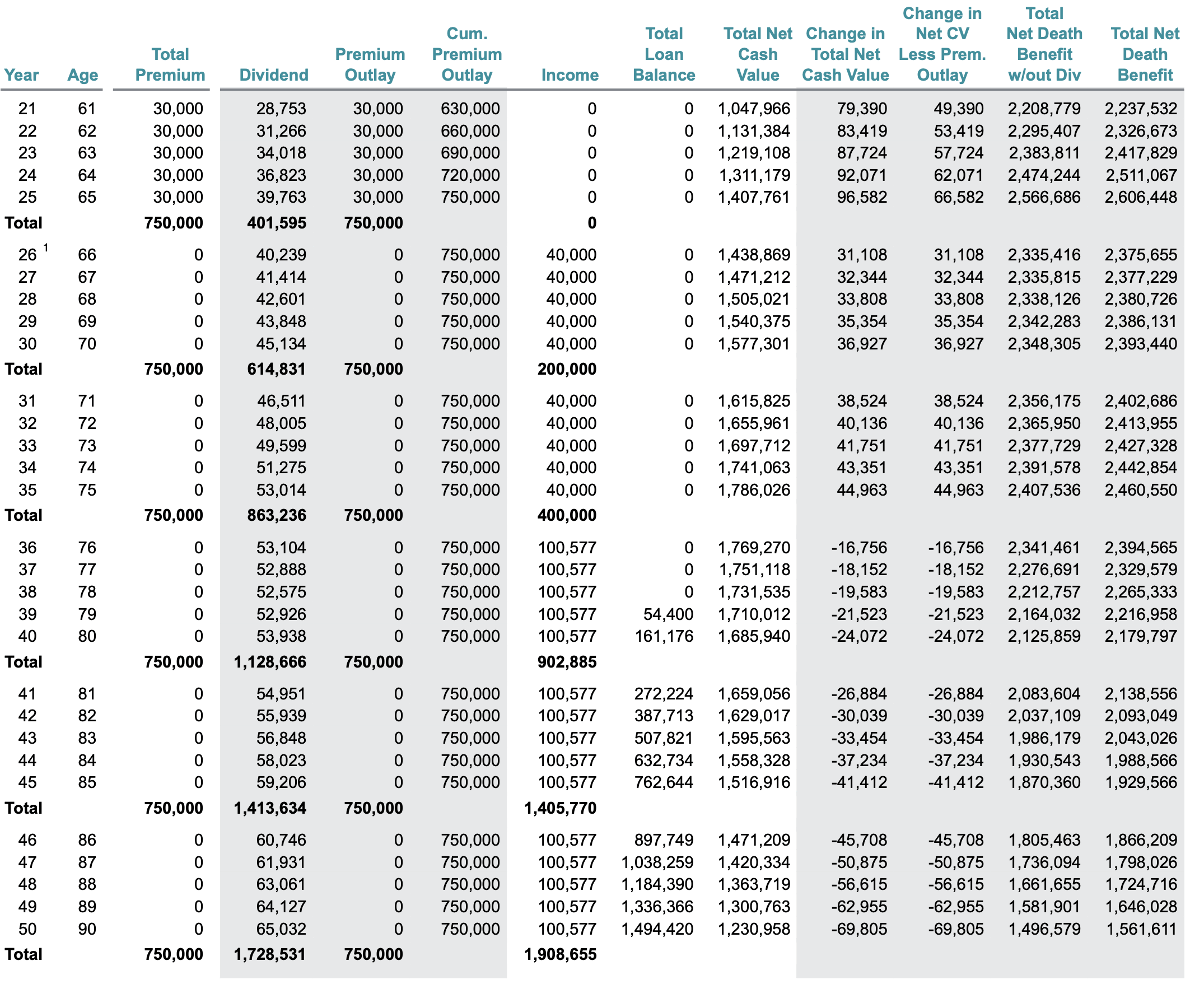

However what if this particular person would not want $72,561 in earnings from his entire life insurance coverage coverage. What if he solely wants $40,000 per yr when retirement begins?

This is what that appears like:

Right here we see if he makes use of his entire life insurance coverage coverage to cowl $40,000 in earnings wants, he may enhance the earnings to $100,577 per yr after the primary 10 years of his retirement. This increased earnings is sustainable–at present dividends–to his age 100.

Utilizing this strategy, at age 100, he’d produce about 15% extra earnings from his coverage versus taking the utmost quantity–$72,561 per yr–starting at retirement and thru his age 100. That distinction in {dollars} is about $375,000.

Entire Life Insurance coverage Revenue is Assured to Get Higher

A few of the extra savvy readers will doubtless suppose to themselves that there is no such thing as a magic right here. In spite of everything, if I’ve $1.4 million in shares and bonds and if I withdraw a low relative quantity towards that steadiness as retirement earnings I can do the identical factor–enhance my earnings later. To this, I’d say, sure…theoretically.

You see shares and bonds may produce the same outcome. If we mannequin one thing utilizing a static charge of return for a hypothetical inventory/bond portfolio that train will definitely inform us this phenomenon exists with that retirement plan as effectively. However the distinction–it is delicate however crucial–is that shares and bonds should not designed to do the identical factor entire life insurance coverage is.

Entire life insurance coverage will enhance over time. It is contractually assured to try this. Yearly you obtain a non-guaranteed outcome with a complete life contract, the resulting guaranteed components enhance for all years moving forward. So taking much less earnings now with the promise of a better earnings capability sooner or later is precisely how entire life insurance coverage works.

Shares and bonds then again solely accomplish this process if the speed of return stays optimistic. This situation enjoying out with shares and bonds can be depending on the timing of returns–maybe we must always name them, the sequence of returns–on the funding. You might need set out in retirement taking an earnings that nobody would deem dangerously excessive. You may also expertise a market correction that brings your account steadiness uncomfortably near requiring a revision to your secure withdrawal charge–maybe one thing persons are coping with as of late–and this is not going to allow a bigger withdrawal charge after years of lesser earnings.

However entire life insurance coverage is totally different. There isn’t a “correction” occasion with entire life insurance coverage. When markets retract, entire life insurance coverage marches ahead, principally unaffected within the interim. Now, massive financial forces can finally affect the general course of the entire life insurance coverage dividend. We witnessed this playout from roughly 2009 by way of the fashionable day. Steady financial “easing” from the Federal Reserve introduced rates of interest to a brand new degree, which finally impacted the dividend funds on entire life insurance coverage. However that took a very long time to materialize–and most dividend-paying whole life insurance policies proceed to compete favorably with comparable risk-profile financial savings plans.

That being mentioned, it is silly to miss the unimpeded progress entire life insurance coverage contracts are designed to have. Taking much less earnings at this time out of your entire life coverage doesn’t sacrifice the utmost you will have obtainable to you. Even when the dividend declines, the assured options of the contract are the first drivers of this attribute.

{kind=link}