An insurance declare comes at a annoying time in a buyer’s life, typically making it a damaging expertise. A minimum of, that’s what you would possibly assume. That’s why I used to be shocked when our newest analysis report, Why AI in Insurance Claims and Underwriting,

Pace of settlement drives claims satisfaction in insurance coverage

General, our survey discovered that 70% of insurance coverage policyholders stated they have been both glad or very glad with how their insurance coverage firm or agent dealt with their declare.

For claims, that is fairly excessive. And our survey just isn’t the one knowledge level to indicate this. A 2021 J.D. Power survey focused on auto insurance confirmed record-high buyer satisfaction on claims, hitting 880 on a 1,000-point scale. An analogous 2021 J.D. Power survey on property claims confirmed a slight dip in satisfaction charges (from 883 to 871), however this broke a 5-year streak of steadily rising satisfaction scores and is probably going as a result of circumstances circuitously associated to insurers (like provide chain disruptions and materials shortages associated to the pandemic). So, what’s inflicting these rising satisfaction charges?

Omnichannel communication and transparency are two causes. Most insurers enable clients to open a declare on an internet site or app. Know-how affords comfort by way of utilizing pictures for an inspection as a substitute of scheduling an individual to come back on-site. And a few insurance coverage corporations supply a dashboard to trace a declare all through its lifecycle.

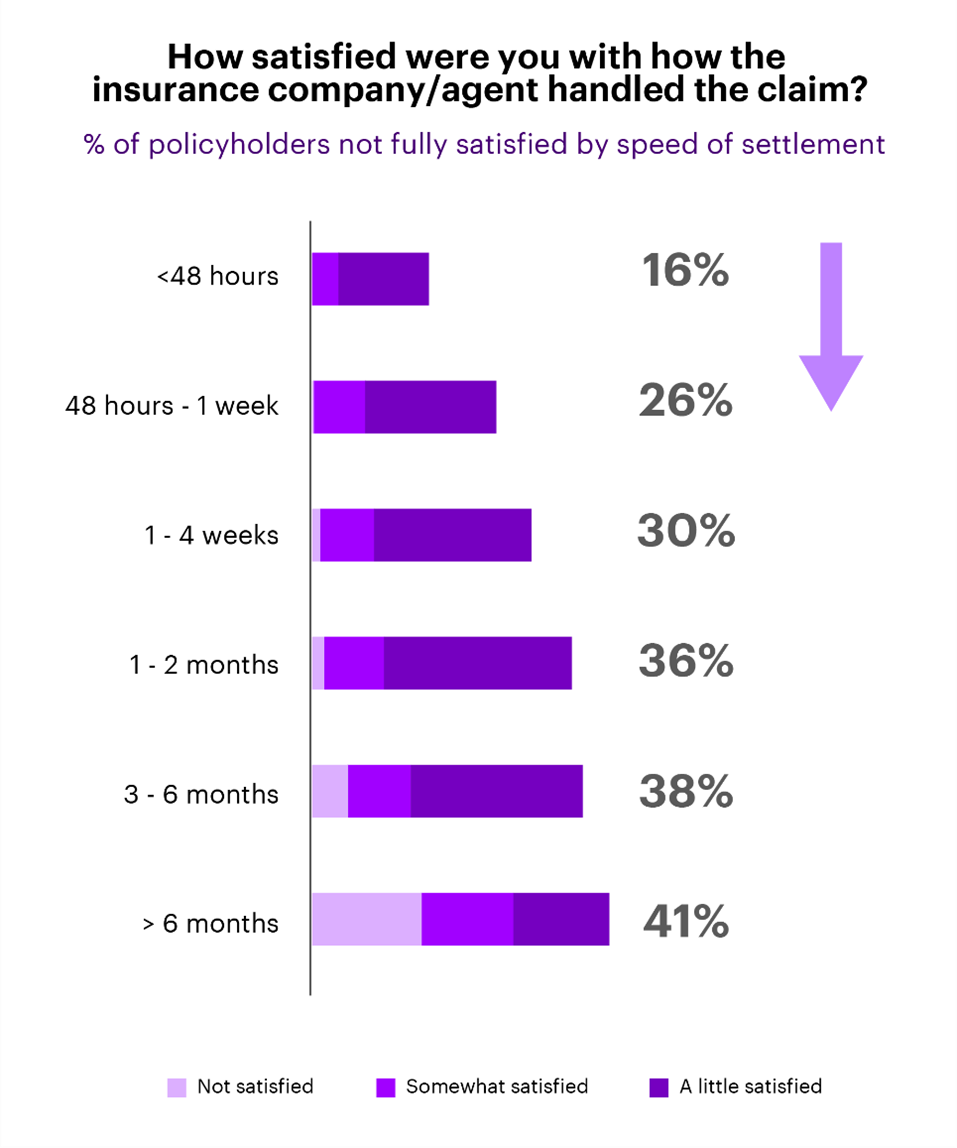

These are all essential modernizations which have helped the claims expertise be extra seamless. Nonetheless, there’s one piece that, in line with our survey, drives satisfaction charges greater than the rest: pace of settlement. The longer it takes to settle a declare, the much less glad that policyholder can be.

This perception is especially essential for insurers, since claims dissatisfaction is a significant factor in driving policyholders to change to a different firm, with 74% of dissatisfied clients both saying they did change suppliers (26%) or are contemplating it (48%).

Insurers ought to concentrate on AI to construct on excessive claims satisfaction charges

Realizing that pace of settlement is a core driver, how do insurers proceed to get excessive ranges of satisfaction and, extra importantly, construct on that?

For a few years, insurers have been targeted on the omnichannel. We’re at some extent now the place continued funding in omnichannel is giving diminishing returns. In fact, this isn’t to say omnichannel ought to be ignored. New routes that concentrate on youthful generations, like chat apps (WhatsApp, and so forth.), will nonetheless be an essential technique for insurers to increase their buyer base. And perfecting or modernizing no matter omnichannel providing insurers at the moment have can be essential to remain related. What I’m saying is that omnichannel is low-hanging fruit—most of which we’ve picked already.

As a substitute, insurers ought to concentrate on AI to automate the settlement course of to be quick, straightforward and correct. In fact, that is simpler stated than carried out. Automating the settlement course of requires strong knowledge and analytics capabilities all related in a single ecosystem.

Disconnect between intention and motion

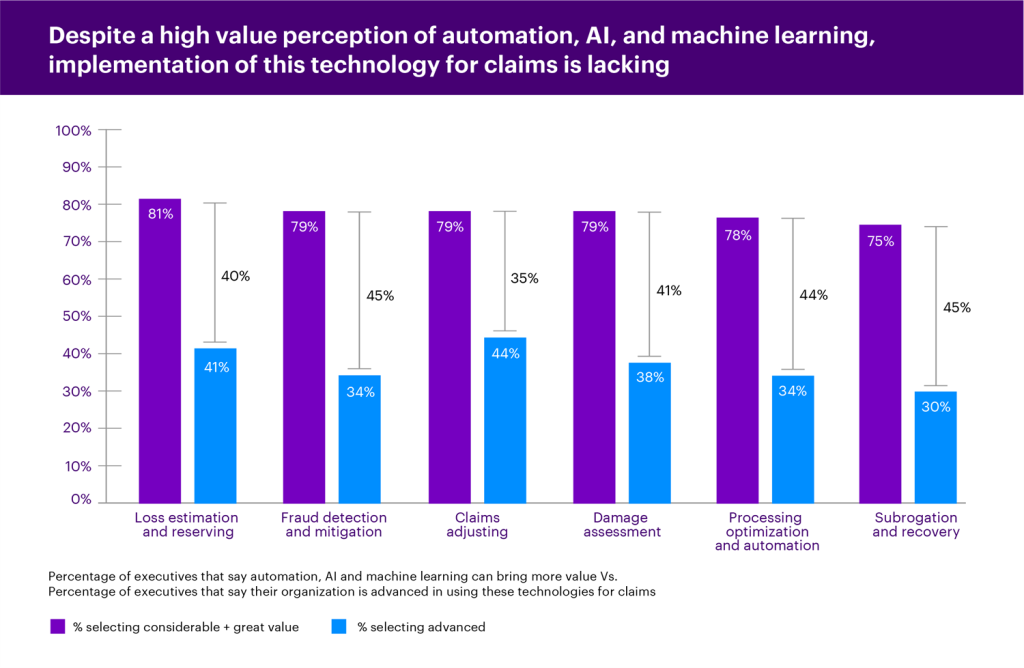

Executives already know the significance of utilizing AI in claims. The graph beneath exhibits that, for every space of the claims worth chain, at the least 75% of executives stated AI and machine studying can carry “appreciable” or “nice” worth.

But, there’s a disconnect between this intention and taking motion. The identical graph exhibits this hole, the place even probably the most superior space (claims adjusting) nonetheless has solely 44% of executives saying they’re superior of their use of AI, automation and machine studying. On this state of affairs, our definition of “superior” is after the extent “utilizing in preliminary levels.”

Insurance coverage executives ought to have a look at priorities holistically

So, about 80% of executives notice the worth of AI in claims, and about 40% think about themselves superior in several areas. Not surprisingly, investments in claims will speed up over the subsequent three years, with 65% of these we surveyed planning to take a position greater than $10 million.

Insurers shouldn’t be discouraged, nevertheless, as a result of pace of settlement priorities align to different govt priorities, similar to decreasing admin prices and plugging claims leakage—and the options are the identical. That’s why executives ought to keep away from attempting to resolve every drawback individually and as a substitute ask how AI, machine studying and different automation can rework the enterprise in a manner that can concurrently hit a number of priorities. For instance, rising pace of settlement by automation will naturally scale back admin prices and keep away from claims leakage, whereas rising buyer satisfaction and retention.

Insurance coverage leaders additionally must be brave to deal with these bigger challenges and keep away from placing an excessive amount of time and power in easier priorities (like omnichannel).

Insurers know the sort of worth AI can supply, however they’re falling behind in implementation. Fortunately, the current surge in direction of the cloud will assist. Cloud is a vital basis to leverage real-time knowledge and modeling that can gas the sort of automation.

General, there’s nonetheless a whole lot of work to do to get know-how platforms to the purpose the place they will automate pace of settlement and higher leverage AI throughout the enterprise. However it’s clear that AI and automation is the place the funding ought to be going for insurers to reap probably the most advantages: glad clients, empowered workers and a extra resilience enterprise. Learn our full report on AI-led Transformation in Insurance to study extra.

Get the most recent insurance coverage trade insights, information, and analysis delivered straight to your inbox.

STANDARD DISCLAIMER:

{kind=link}