Life insurance coverage has earned a well-deserved popularity as some of the tax-advantaged monetary automobiles accessible. The power to develop money worth tax-deferred and entry it tax-free has made whole life and universal life insurance coverage in style decisions for constructing wealth. Nevertheless, it is essential to know that not each life insurance coverage transaction is tax-free.

As somebody who has helped numerous shoppers navigate the complexities of life insurance coverage taxation, I wish to share six particular conditions the place your life insurance coverage coverage may create sudden tax penalties. Understanding these situations will allow you to keep away from pricey errors and make knowledgeable choices about your coverage.

1. Withdrawing Money Worth Past Your Price Foundation

The commonest taxable occasion happens while you withdraw extra out of your coverage than you have paid in premiums. Here is the way it works:

While you pay premiums into your life insurance coverage coverage, you create what’s referred to as a “value foundation” or “tax foundation” within the contract. This represents the after-tax {dollars} you have invested within the coverage. One of many stunning options of life insurance coverage is that you could withdraw your value foundation fully tax-free earlier than touching any good points.

The Drawback: In the event you withdraw past your value foundation, these distributions grow to be taxable as bizarre earnings—not capital good points. This distinction is essential as a result of bizarre earnings tax charges are usually greater than capital good points charges, no matter how lengthy you have owned the coverage.

What makes this worse: As soon as you are taking a withdrawal, you usually cannot reverse it. In the event you notice you have made a mistake and withdrawn acquire as a substitute of foundation, you possibly can’t merely put the cash again.

The right way to keep away from it: At all times verify along with your insurance coverage firm to verify your present value foundation earlier than taking any withdrawals. In the event you’ve exhausted your value foundation, take into account taking a coverage mortgage as a substitute, which does not create instant tax legal responsibility.

The Hidden Dividend Entice

Many policyholders unknowingly create tax issues by selecting to obtain dividends as cash payments. Every money dividend cost reduces your value foundation. In the event you’re not at the moment paying premiums (resembling with a paid-up coverage), you don’t have any strategy to restore this foundation.

Over time, particularly with paid-up insurance policies, you possibly can exhaust your complete value foundation by means of dividend funds alone. As soon as this occurs, all future dividend funds grow to be taxable as bizarre earnings.

Professional tip: Dividend elections are usually locked in for all the coverage yr, so you possibly can’t change them mid-year even should you notice a tax drawback is coming.

Accumulating Dividends at Curiosity

In the event you select the dividend choice to “accumulate at curiosity,” bear in mind that the curiosity earned on these collected dividends is taxable as bizarre earnings. This money sits outdoors your life insurance coverage coverage and would not take pleasure in the identical tax advantages as money worth contained in the coverage.

2. Surrendering Your Coverage

While you surrender (cancel) your life insurance coverage coverage, any money worth above your value foundation turns into taxable as bizarre earnings. Whereas this might sound simple, there are a number of refinements that may catch you off guard:

- Sure coverage riders could not rely towards your value foundation

- The insurance coverage firm’s information of your value foundation could differ out of your calculations

- If the insurance coverage firm takes longer than required to pay your give up worth, they’re going to add curiosity—which can also be taxable

Essential level: The insurance coverage firm will use their information to arrange the 1099 type despatched to the IRS. Ensure you know what they’ve on file to your value foundation earlier than surrendering.

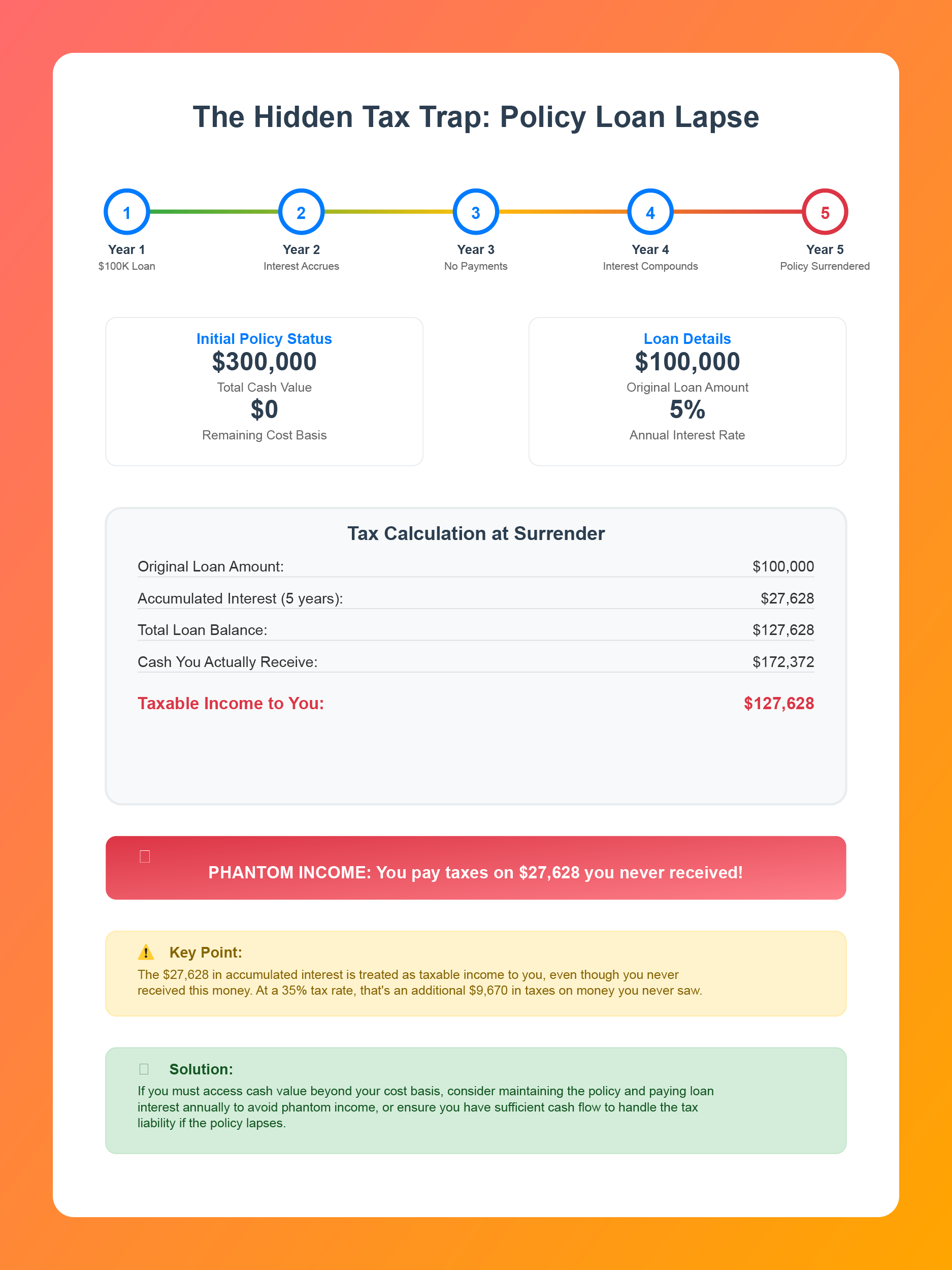

3. Coverage Loans Gone Flawed

Policy loans are sometimes touted as a tax-free strategy to entry your money worth, and they are often—however provided that your coverage stays in pressure till you die. In case your coverage lapses otherwise you give up it with an excellent mortgage, the mortgage quantity (together with collected curiosity) turns into a taxable distribution.

Here is a real-world instance: Suppose you will have a coverage with no remaining value foundation and $300,000 in money worth. You’re taking a $100,000 mortgage at 5% curiosity. 5 years later, you resolve to give up the coverage with out having made any mortgage funds. The collected curiosity is almost $30,000, which implies:

- You obtain $30,000 much less money from the insurance coverage firm

- You continue to owe taxes on that $30,000 as if it had been earnings, despite the fact that you by no means obtained it

This “phantom earnings” situation can create a major tax burden.

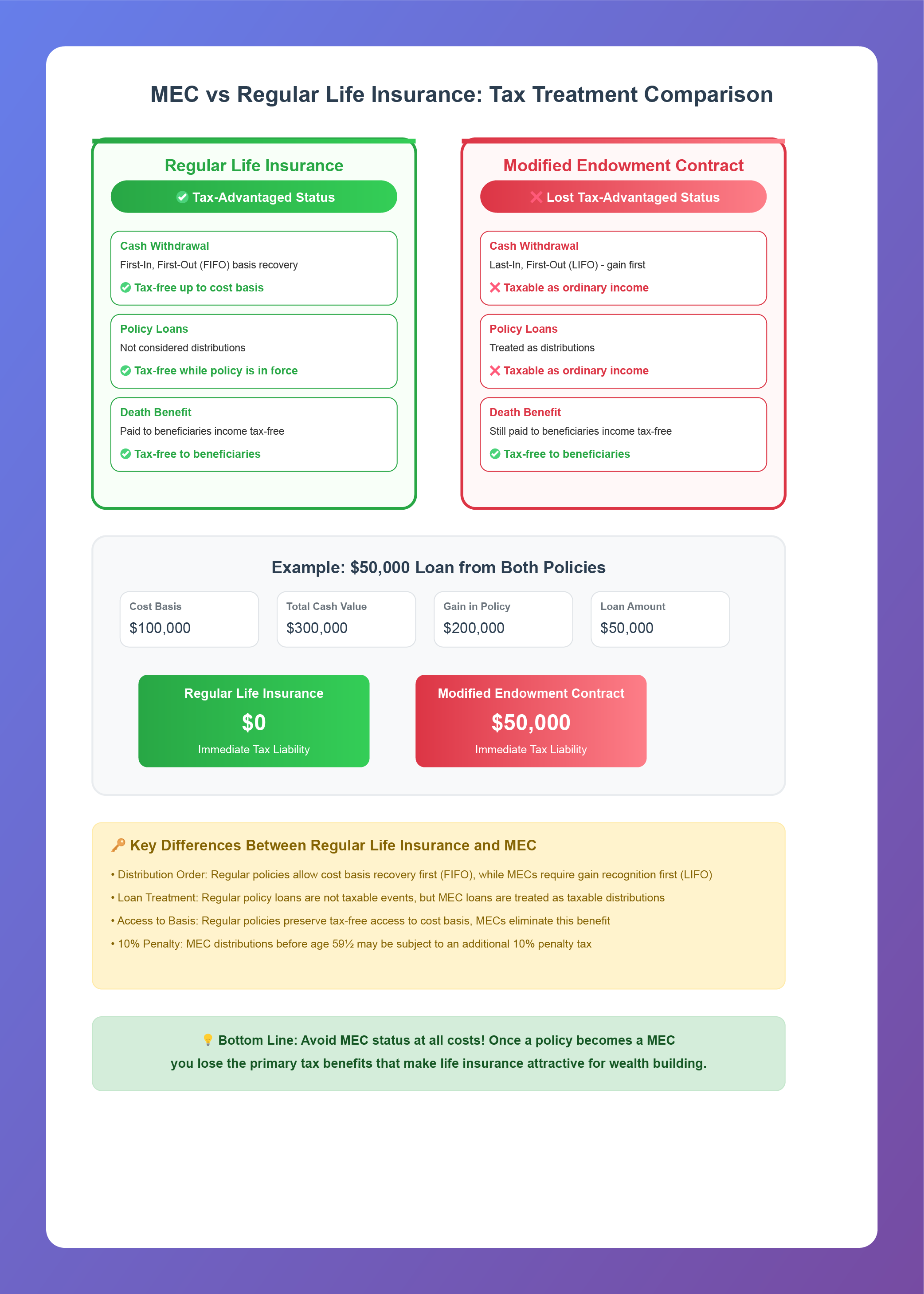

4. Modified Endowment Contracts (MECs)

In case your life insurance coverage coverage loses its life insurance coverage standing and turns into a Modified Endowment Contract (MEC), the tax guidelines change dramatically:

- You lose the flexibility to withdraw your foundation first

- All distributions (together with loans) are taxed as bizarre earnings till you have withdrawn all of the acquire

- There is no distinction between withdrawals and loans for tax functions

Instance: With a MEC having $100,000 in value foundation and $300,000 complete money worth (so $200,000 in acquire), a $50,000 mortgage would create $50,000 of taxable earnings instantly, plus any curiosity that accumulates in the course of the tax yr.

5. Dying Profit Issues

Whereas dying advantages are usually earnings tax-free to beneficiaries, sure decisions can create tax legal responsibility:

Life Settlement Choices

When beneficiaries select to obtain dying advantages in installments relatively than a lump sum, the insurance coverage firm holds onto a part of the cash and pays curiosity on it. This curiosity is taxable as bizarre earnings.

Retained Earnings Accounts

Many insurance coverage firms supply beneficiaries the choice to maintain dying profit proceeds in an account with check-writing privileges. These accounts typically pay engaging rates of interest, however that curiosity is taxable as bizarre earnings.

Property Tax Issues

Whereas dying advantages are earnings tax-free, they don’t seem to be essentially transfer tax-free. For big estates, life insurance coverage proceeds are usually included within the property for tax functions except the coverage is owned by an irrevocable belief.

6. 1035 Change Boot Earnings

Essentially the most advanced tax lure includes 1035 exchanges with excellent loans. Here is a situation that journeys up many policyholders:

You’ve a coverage with an excellent mortgage and wish to alternate it for a brand new coverage by way of a 1035 alternate. The brand new insurance coverage firm will not help you switch the mortgage, so that you resolve to give up sufficient money worth to repay the mortgage after which switch the remaining money to the brand new coverage.

The issue: This creates “boot earnings”—taxable earnings that arises while you give up money worth to repay a mortgage as a part of a 1035 alternate.

Options:

- Use cash from outdoors the coverage to repay the mortgage

- Repay the mortgage by means of give up, however wait a minimum of 12 months earlier than making the alternate

- Discover an insurance coverage firm that may settle for the mortgage switch

Key Takeaways

Life insurance coverage stays some of the tax-advantaged monetary instruments accessible, however it’s not foolproof. The important thing to avoiding these tax traps is knowing the foundations and planning accordingly:

- Monitor your value foundation frequently, particularly should you take dividends as money

- Seek the advice of along with your insurance coverage firm earlier than making any withdrawals or adjustments

- Keep away from letting insurance policies lapse with excellent loans

- Be cautious with 1035 exchanges involving loans

- Contemplate skilled steerage for advanced conditions

Bear in mind, all taxable occasions associated to life insurance coverage are handled as bizarre earnings, not capital good points. This makes the tax chunk doubtlessly extra extreme than different funding automobiles.

The objective is not to keep away from life insurance coverage due to these potential tax points—it is to know them so you possibly can navigate round them and proceed to profit from this highly effective wealth-building device.

This info is for academic functions solely and shouldn’t be thought-about tax recommendation. At all times seek the advice of with a professional tax skilled earlier than making choices that would have an effect on your tax state of affairs.

{kind=link}

После обращения пациента в клинику «НаркоЩит» наш специалист выезжает на дом в течение 30–60 минут. По прибытии врач проводит подробный осмотр: измеряет артериальное давление, пульс и уровень кислорода в крови, а также собирает анамнез, чтобы оценить степень интоксикации и тяжесть запоя. На основе полученной информации формируется индивидуальный план лечения.

Детальнее – http://kapelnica-ot-zapoya-nizhniy-novgorod00.ru/kapelnicza-ot-zapoya-na-domu-nizhnij-novgorod/

Great information shared.. really enjoyed reading this post thank you author for sharing this post .. appreciated

Business car rentals, on advantageous conditions.

honda rental car price [url=https://neochorion.com /our-cars/?view=cardetails&carid=9/]https://neochorion.com /our-cars/?view=cardetails&carid=9/[/url] .

ремонт телевизоров тошиба [url=https://toshiba-servisnyj-centr.ru/]ремонт телевизора toshiba[/url] – профессиональный ремонт с гарантией качества.