As shoppers face decreased entry to Market medical insurance subsidies for 2026 plans – and better web premiums for shoppers who proceed to be subsidy-eligible – one clear shopping for pattern has emerged: a migration of patrons to Bronze-level well being plans.

Whereas particulars in regards to the plans that folks chosen for 2026 will not be but out there in most states, a number of state-run Marketplaces have revealed this info in early 2026. Knowledge from these state-run exchanges exhibits a major variety of enrollees have downgraded their protection, choosing a Bronze plan as a substitute of a Gold or Silver plan.

What’s occurring with Market well being plan enrollments?

Enrollment in Market well being plans declined in 2026 after 4 consecutive years of record-high enrollment. This was not stunning, given the sharp increase in net premiums for 2026 due to the expiration of federal subsidy enhancements on the finish of 2025.

We don’t but have Market metal-level plan choice information for the states that use HealthCare.gov, however about half of the state-run Marketplaces have shared details about the steel ranges that folks chosen throughout open enrollment. Usually, Bronze plan picks elevated considerably. (There have been a few exceptions, which we’ll focus on in a second.)

Why would possibly shoppers be downgrading to Bronze plans?

Decrease premiums

Though all Market plans cowl the ACA’s important well being advantages, Bronze plans have increased deductibles and out-of-pocket limits than Silver or Gold plans. Consequently, Bronze plans have decrease month-to-month premiums.

So when shoppers had been confronted with common web premiums that greater than doubled for 2026, it’s comprehensible that folks could have chosen a special plan with a decrease premium, in an effort to maintain their month-to-month premium prices reasonably priced.

Entry to HSA contributions

The truth that Bronze plans are newly HSA-eligible can also have been a think about some enrollees’ choices to downgrade to a Bronze plan. As of 2026, all Bronze (and Catastrophic) Marketplace plans are HSA-eligible, that means that individuals who enroll in these plans have the choice to contribute pre-tax cash to a well being financial savings account (HSA).

Learn more about health savings accounts and the tax advantages they offer.

Contributions to an HSA will scale back the ACA-specific modified adjusted gross income (MAGI) that’s used to find out Market subsidy eligibility. So deciding on an HSA-eligible plan and making HSA contributions is a means for individuals to increase their subsidy amount (because of their diminished MAGI) or doubtlessly qualify for subsidies if the HSA contribution brings their MAGI down under 400% of the federal poverty stage (FPL).

This grew to become extra necessary in 2026, because of the return of the “subsidy cliff.” Enrollees with family revenue above 400% of FPL should pay full-price for his or her protection in 2026, so choosing a Bronze plan and contributing to an HSA could have been a selection that allowed some enrollees to proceed to qualify for a subsidy.

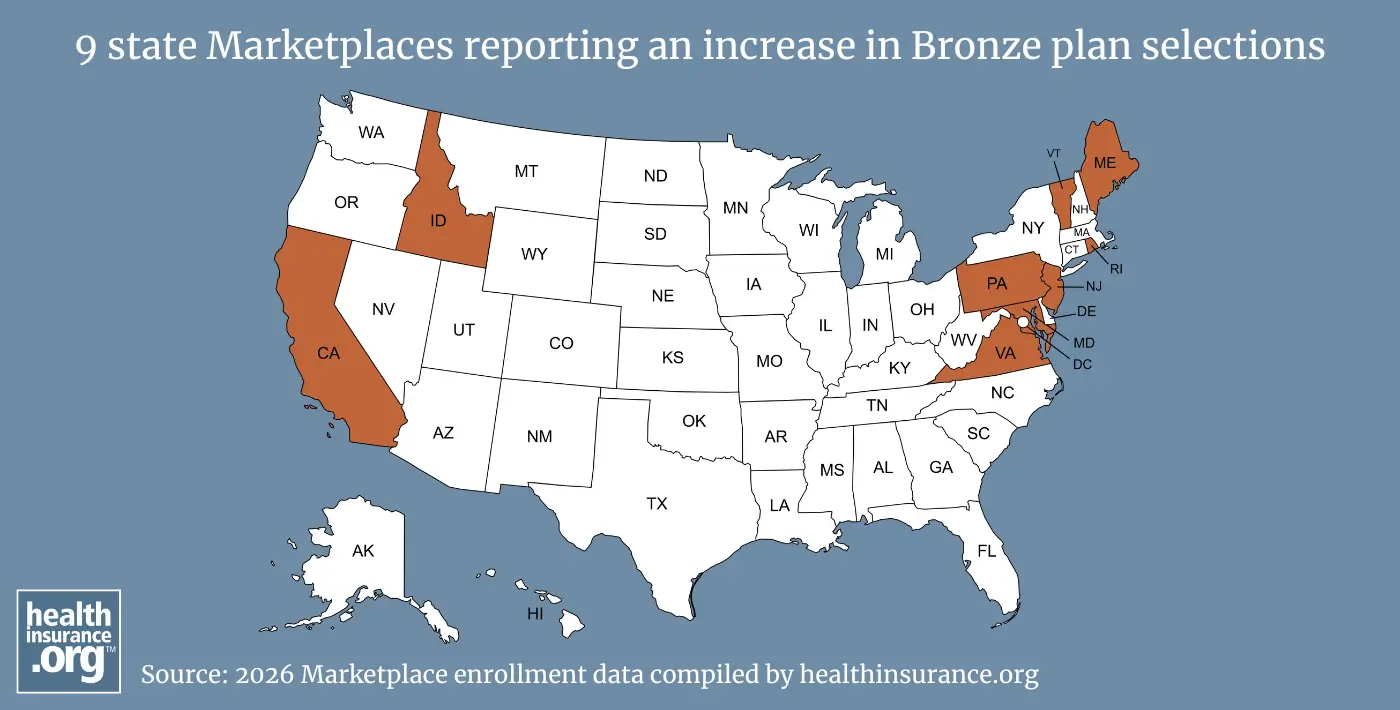

Which state-run Marketplaces have reported a rise in Bronze plan picks?

Of the state-run Marketplaces which have revealed 2026 enrollment metrics up to now, all however two have reported a rise within the proportion of enrollees deciding on Bronze plans:

- California: Of enrollees in 2025 plans, 130,000 enrollees switched to Bronze plans for 2026. And amongst new enrollees, greater than a 3rd chosen Bronze plans, in contrast with fewer than 1 / 4 final yr.

- Idaho: Practically 60% of enrollees picked Bronze plans, whereas enrollment in Silver and Gold plans declined in comparison with 2025 enrollment.

- Maine: Practically 60% of enrollees picked Bronze plans – up from 46% in 2025. (The proportion of enrollees in Bronze plans had been fairly regular from 2022 by 2025.)

- Maryland: The change reported that 5,743 individuals switched from 2025 Gold plans to Bronze plans for 2026.

- New Jersey: Amongst individuals who actively chosen a plan (not counting auto-renewals), 31% selected a Bronze plan, up from 16% the yr earlier than.

- Pennsylvania: Bronze plan picks had been 30% increased than they had been the yr earlier than.

- Rhode Island: As of mid-January 2026, about 38% of latest enrollees had picked a Bronze plan, up from about 15% in earlier years. There was additionally a pattern of current enrollees switching to Bronze plans at that time.

- Vermont: Nearly twice as many individuals newly chosen a Bronze plan for 2026, in contrast with 2025. And greater than 60% of the brand new Bronze enrollees had beforehand been enrolled in Gold plans.

- Virginia: Bronze plan picks elevated, though not as considerably as they did in many of the different states listed above. For 2026 protection, 42% of enrollees chosen Bronze plans, up from 38% in 2025.

4 of these 9 states (California, Maryland, New Jersey, and Vermont) provide state-funded subsidies in addition to federal subsidies, in an effort to make Market protection extra reasonably priced. However regardless of this extra help, a major variety of enrollees nonetheless downgraded their protection for 2026.

Which state-run Marketplaces reported a discount in Bronze plan picks?

Two state-run Marketplaces have reported a lower in Bronze plan picks for 2026. In each instances, the state had taken action to make more robust coverage more affordable for residents:

New Mexico

Only a few Market enrollees in New Mexico have Bronze plans. Enrollment in Bronze plans dropped barely – from 3.4% in 2025 to three.1% in 2026.

New Mexico gives further state-funded subsidies that end in sturdy “Turquoise” plans being out there to enrollees with family incomes as much as 400% of the federal poverty stage. These are by far the most well-liked plans within the New Mexico Market, chosen by practically eight out of ten enrollees shopping for 2026 plans.

New Mexico can also be the one state that used state funding to totally backfill the discount in federal premium subsidies for 2026. So whereas shoppers in lots of states responded to increased web premiums (stemming from the expiration of the federal subsidy enhancements) by downgrading their protection to a plan with a decrease premium, there was no want for New Mexico residents to try this.

Washington

About 87,000 Washington Market enrollees chosen Bronze plans for 2026, versus about 96,000 who had picked Bronze plans for 2025. (In each instances, this was roughly three out of ten enrollees, since whole enrollment declined for 2026.)

However Gold plan picks elevated considerably in Washington, growing from 18% of plan picks in 2025 to 53% in 2026.

This migration to Gold plans occurred as a result of Washington adopted premium alignment for 2026, requiring insurers so as to add a 43% load to the premiums for Silver plans. It is because most Silver plans even have advantages which are just like these of Platinum plans, on account of cost-sharing reductions (CSR).

As a result of Silver plans grew to become costlier, premium subsidies additionally elevated, as subsidy quantities are based mostly on the price of a Silver plan. These bigger subsidies made Gold plans extra reasonably priced, resulting in a considerable enhance in Gold plan picks for 2026.

What does a shift to Bronze plans imply for shoppers?

Bronze plans have common deductibles of practically $7,500 in 2026, which is greater than double the general weighted common deductible throughout all Market plans. Plan designs differ significantly, however some Bronze plans rely all non-preventive care towards the deductible (and deductibles will be as excessive as $10,600 in 2026, relying on how the plan is designed).

So shoppers who choose Bronze plans will usually have deductibles which are fairly a bit increased than the typical Market plan deductible. Their whole out-of-pocket publicity is usually as excessive because the allowable most, which is $10,600 for a single individual in 2026. And relying on how the plan is designed, it’d pay little or no till the enrollee has met the deductible.

This implies Bronze plan enrollees must be ready for the opportunity of having to pay a number of thousand {dollars} in out-of-pocket prices in the event that they find yourself needing medical care throughout the yr.

Sadly, an individual who downgraded to a Bronze plan due to premium affordability would possibly wrestle to give you the cash to pay their deductible. Or they could keep away from getting mandatory medical care due to the price.

Choices for Bronze plan patrons going through increased out-of-pocket prices

Should you’re enrolled in a Bronze plan and nervous about increased out-of-pocket prices, there are a number of suggestions to remember:

- Comparability store to your care at any time when attainable. Though your well being plan may need a variety of in-network hospitals, medical workplaces, and pharmacies, that doesn’t imply your out-of-pocket prices would be the identical in any respect of them. Should you want a prescription, you may examine with numerous in-network pharmacies (together with mail-order choices) to see if there are value variations. The identical is true for different medical care, and there are transparency instruments that may assist you to decide what your prices will likely be.

- Focus on your monetary scenario together with your medical suppliers. It’s possible you’ll discover that they’ll provide a fee plan that matches inside your price range.

- If in any respect attainable, think about opening and funding an HSA. All Bronze plans are HSA-eligible as of 2026. The cash you contribute to an HSA is pre-tax. And if you must use it to pay your deductible or different medical bills, it can proceed to be tax-free while you make the withdrawal. Should you don’t find yourself needing to make use of the cash in your HSA, it can stay within the account in future years till if and while you want it.

- In case your revenue isn’t greater than 200% of the federal poverty stage, you could be eligible for diminished out-of-pocket prices when you use a federally qualified health center (FQHC) that’s in your plan’s supplier community. Relying in your revenue, these clinics can scale back the quantity that you simply’d in any other case should pay out-of-pocket below the phrases of your well being plan.

- Contemplate supplemental coverage, akin to a critical illness policy or an accident insurance policy, that would reimburse a few of your out-of-pocket prices when you had been to face sudden medical prices for a coated sickness or harm.

- Some individuals with high-deductible medical insurance select to enroll in an area physician’s direct primary care (DPC) membership program, to have limitless entry to numerous main care companies. And as of 2026, having a DPC membership not prohibits an individual from making HSA contributions if additionally they have an HSA-eligible well being plan, so long as the DPC membership meets sure parameters.

Louise Norris is a person medical insurance dealer who has been writing about medical insurance and well being reform since 2006. She has written a whole lot of opinions and academic items in regards to the Inexpensive Care Act for healthinsurance.org.

[author_name]

{kind=link}