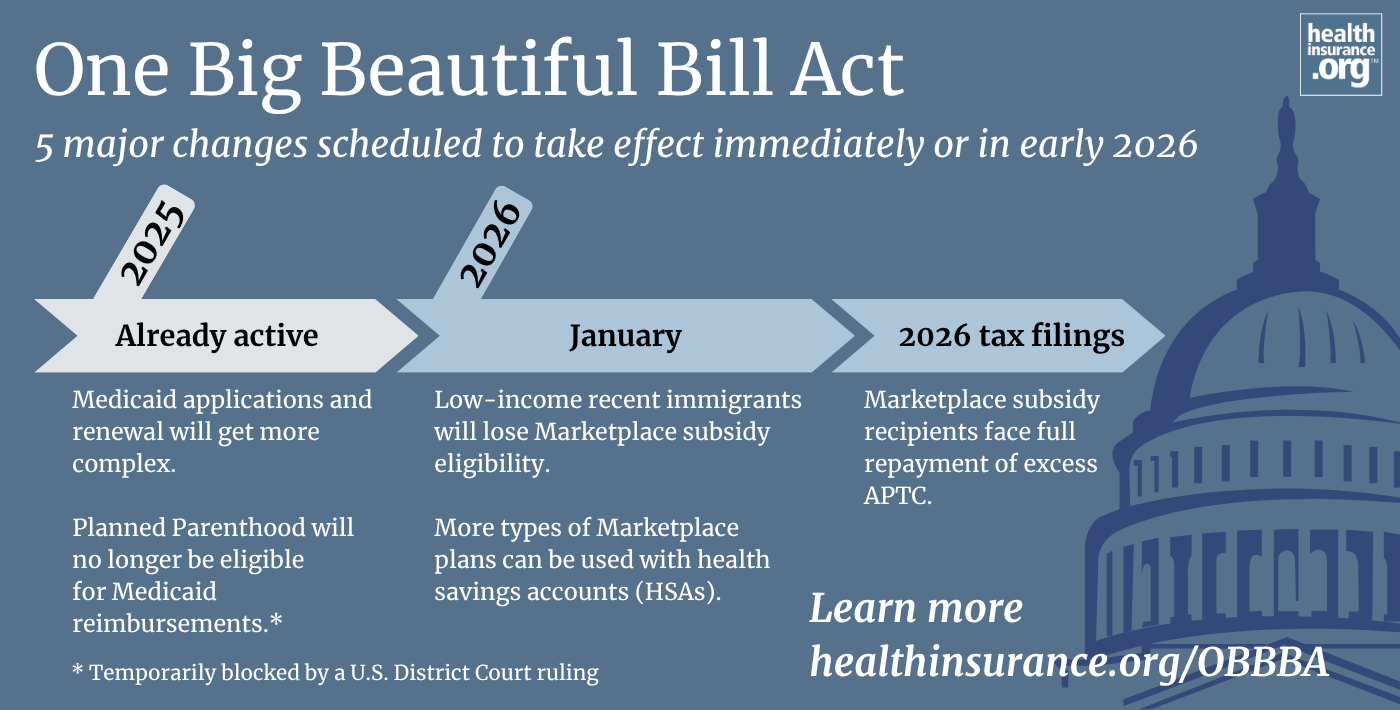

The One Massive Stunning Invoice Act (OBBBA) – or H.R. 1 – has set the stage for sweeping modifications to U.S. well being protection, lots of which received’t take impact till 2027 or later. However some modifications are occurring a lot sooner – beginning proper now, later in 2025 and early 2026 – and can considerably impression Medicaid enrollees, Market customers, and low-income immigrants.

On this article, we have a look at 5 main modifications for customers to look at, a few of which take impact instantly.

What’s the OBBBA?

President Donald Trump signed into regulation the OBBBA, which is federal price range laws, on July 4, 2025. The laws may have important implications for well being protection in america within the coming years. Thousands and thousands of persons are anticipated to lose protection, due largely to the Medicaid modifications that will probably be carried out in 2027 and future years.

And that is along with the tens of millions of people who find themselves anticipated to lose well being protection because of the anticipated sunsetting of the Marketplace subsidy enhancements at the end of 2025 and the brand new Marketplace rules that were finalized in 2025. Altogether, the variety of uninsured folks within the U.S. is predicted to extend by about 17 million folks within the subsequent decade or so, because of the One Massive Stunning Invoice, the expiration of the subsidy enhancements, and the brand new Market guidelines.

However though most of the One Massive Stunning Invoice’s coverage modifications received’t take impact till 2027 or later, a few of the regulation’s Medicaid and Market modifications will probably be carried out by the point open enrollment for 2026 protection begins in November 2025.

Right here’s what customers have to know, and the way their well being protection choices could possibly be affected:

1. Medicaid purposes and renewal will get extra complicated

- In a nutshell: Medicaid enrollees will face extra administrative hurdles when making use of for or renewing protection.

- Who’s affected? Medicaid and CHIP enrollees – together with these in Medicare Financial savings Packages (MSPs) – and particularly older adults and other people with disabilities.

- Takes impact: July 4, 2025

In 2023 and 2024, the Biden administration finalized a two-part rule designed to simplify and streamline the appliance and renewal course of for Medicaid (together with Medicare Financial savings Packages, which help to pay Medicare premiums and out-of-pocket costs for beneficiaries with low incomes and asset ranges), the Youngsters’s Well being Insurance coverage Program (CHIP), and Fundamental Well being Packages.

The Biden administration’s rule included provisions akin to eliminating in-person eligibility interviews for folks with disabilities and people 65 or older, modifications to make sure that fewer folks would lose protection attributable to undeliverable mail, and a ban on lock-out intervals for youngsters disenrolled from CHIP for failure to pay premiums.

Beginning instantly, H.R.1 prohibits the Division of Well being and Human Companies (HHS) from implementing, administering, or implementing that rule, not less than by way of September 2034.

As is the case for different Medicaid cuts within the One Massive Stunning Invoice, sources undertaking these modifications will result in a lower in federal Medicaid spending, attributable to fewer folks being enrolled in this system.

What folks affected by the change can do: With a view to enroll in and renew protection, folks might discover that they should full further paperwork or adjust to different new guidelines. If you happen to’re enrolled in Medicaid (together with an MSP) or CHIP, it’s important to ensure that the state Medicaid company has your appropriate contact data, and that you just shortly reply to any administrative requests associated to your eligibility or protection renewal.

2. Deliberate Parenthood not eligible for Medicaid reimbursements

- In a nutshell: Medicaid can not reimburse the prices of any well being care offered at Deliberate Parenthood or different “important neighborhood suppliers” that provide abortion care.

- Who’s affected? Deliberate Parenthood clinics and comparable “important neighborhood suppliers,” and Medicaid enrollees who obtain any sort of well being care at these clinics.

- Takes impact: July 4, 2025 (quickly blocked by a courtroom ruling)

As quickly because it was enacted, the OBBBA eradicated Medicaid funding for one 12 months, for entities which are “primarily engaged in household planning companies, reproductive well being, and associated medical care” and that present abortion companies in conditions aside from rape, incest, or a hazard to the mom’s life.

It’s vital to notice that longstanding federal guidelines already prevent federal funding from being used to pay for abortion care, besides when the abortion stems from rape, incest, or a hazard to the mom’s life. (Thus, non-excepted abortions, dubbed “non-Hyde” abortions, can’t be funded with federal cash.) So the change beneath the OBBBA ends in federal Medicaid funding being reduce for non-abortion care, akin to most cancers screenings and contraception.

This resulted in some Deliberate Parenthood clinics notifying sufferers that they may not settle for Medicaid.

However Deliberate Parenthood instantly filed a lawsuit to dam the Medicaid funding reduce, and a decide issued a 14-day injunction on July 7, quickly blocking the Division of Well being & Human Companies from chopping off Medicaid funding to Deliberate Parenthood.

The governor of Washington introduced that if Deliberate Parenthood’s lawsuit to completely block the funding reduce is unsuccessful, the state of Washington will cowl the $11 million in federal Medicaid funding that Deliberate Parenthood will lose in Washington. As famous above, federal funding can’t be used for non-Hyde abortions, in order that $11 million is for different medical companies, akin to preventive care.

3. Low-income immigrants will lose subsidy eligibility

- In a nutshell: Lately arrived low-income immigrants will not qualify for subsidies to purchase Market medical insurance.

- Who’s affected? Lawfully current immigrants of their first 5 years within the U.S. with family incomes beneath the federal poverty stage.

- Takes impact: January 1, 2026

Generally, Market subsidies usually are not out there to anybody with a family revenue beneath the federal poverty stage (FPL). However there has at all times been an exception for current immigrants who’re lawfully current within the U.S. if they’re within the five-year ready interval earlier than they’ll qualify for Medicaid.

To keep away from making a protection hole for low-income lawfully current immigrants throughout their first 5 years within the U.S., the Reasonably priced Care Act (ACA) included a provision to permit them to qualify for Market subsidies so they may meaningfully entry the Market.

However the OBBBA ends this provision, beginning January 1, 2026. Immigrants with family revenue beneath the poverty stage who’ve been within the U.S. for lower than 5 years will not qualify for subsidies within the Market.

In response to the Congressional Price range Workplace, about 300,000 folks will lose their well being protection on account of the termination of subsidy eligibility for current immigrants whose revenue is beneath the FPL.

What folks affected by the change can do: To qualify for Market subsidies, immigrants who’ve been within the U.S. for beneath 5 years will want a family revenue for 2026 that’s not less than equal to the 2025 FPL. In all however Alaska and Hawaii (the place the FPL is greater), that’s $15,650 for a single particular person and $32,150 for a family of 4.

When candidates enroll in Market protection, they’re requested to undertaking their family revenue for the total 12 months that the protection will probably be in impact, so current immigrants who’re enrolling or renewing protection in the course of the open enrollment interval within the fall of 2025 might want to undertaking an revenue of not less than the 2025 FPL after they apply for his or her 2026 subsidies.

And candidates must be ready to supply proof of their revenue after they enroll in or renew their protection for 2026, as that will be required if the applicant attests to an revenue that doesn’t match the knowledge the Market will get from different sources just like the IRS.

4. Subsidy recipients face full reimbursement of extra APTC

- In a nutshell: Beginning with 2026 protection, there’s no restrict on how a lot extra APTC a Market enrollee might need to repay if their revenue finally ends up greater than anticipated.

- Who’s affected? Market enrollees who obtain advance premium tax credit (APTC) – particularly these with revenue fluctuations.

- Takes impact: Applies to 2026 tax filings (primarily based on 2026 protection)

Most Market enrollees – 92% in 2025 – qualify for advance premium tax credit (APTC). APTC is predicated on an applicant’s projected revenue for the related calendar 12 months. The federal authorities advances the estimated premium tax credit score on the applicant’s behalf, to their well being insurer, all year long.

However the next 12 months, that APTC must be reconciled when the enrollee recordsdata their tax return for the 12 months. If the revenue an enrollee earns in the course of the 12 months doesn’t match what they projected after they enrolled, the IRS may owe them further premium tax credit score, or the enrollee might need to pay again a few of the extra APTC that was paid on their behalf.

Till now, there was a cap on how a lot extra APTC folks must repay, so long as their family revenue was lower than 400% of FPL. The particular quantities have been listed annually by the IRS, however probably the most an individual must repay in extra APTC for 2024 was $3,150, if their family revenue was as excessive as 399% of FPL.

However the One Massive Stunning Invoice Act eliminates these caps. Beginning with the 2026 plan 12 months, in case your revenue finally ends up being greater than you projected, there’ll not be a restrict on how a lot extra APTC you need to repay. As a substitute, you’ll have to repay all the extra, no matter how a lot that’s.

For the 2023 tax 12 months, throughout all tax returns that had been filed by late July 2024, a complete of greater than 4.9 million tax filers owed a mixed complete of greater than $6 billion in extra APTC. That’s a median of about $1,224 per filer, though that quantity is after making use of the reimbursement caps, which could possibly be as little as $375 for a single filer in 2024.

(To make clear, the reimbursement caps for 2024 ranged from $375 for a single filer whose family revenue was beneath 200% of FPL, to $3,150 for a household with a family revenue of 399% FPL. The small print are proven in Desk 5 of the IRS directions for Type 8962, which is used to reconcile Market premium tax credit.)

What folks affected by the change can do: When folks enroll in Market protection for 2026, will probably be important to undertaking revenue as precisely as doable. The Market will ask for proof of revenue if the projection you provide doesn’t match what the knowledge the Market will get from knowledge sources just like the IRS.

It should even be a good suggestion to double-check your revenue projection mid-way by way of 2026, to see when you’re on monitor to earn roughly the quantity you projected while you enrolled. If not, you possibly can replace your revenue in your Market account, they usually’ll regulate your subsidy in actual time. This might assist to keep away from having to repay extra APTC while you file your 2026 tax return, which will probably be significantly vital as soon as there’s not a cap on how a lot extra APTC must be repaid.

5. Extra Market plans can be utilized with well being financial savings accounts (HSAs)

- In a nutshell: Thousands and thousands extra folks with high-deductible Market plans will turn out to be eligible to contribute to well being financial savings accounts.

- Who’s affected? Market enrollees with Bronze or Catastrophic plans and customers utilizing direct main care (DPC)

- Takes impact: January 2026 (for 2026 plan 12 months)

Beginning with the 2026 plan 12 months, Market enrollees with Bronze or Catastrophic plans will probably be eligible to contribute to a well being financial savings account (HSA). By the top of 2025, HSA contributions can solely be made by somebody who has an HSA-qualified high-deductible well being plan (HDHP), as outlined by the IRS. However beginning with the 2026 plan 12 months, the HDHP definition will broaden to incorporate all Market Bronze and Catastrophic plans.

Previous to 2026, most Bronze plans usually are not HDHPs, since most Bronze plans don’t meet the present IRS HDHP necessities. For instance, in Chicago, there are 31 Bronze Market plans out there in 2025, however zero HDHPs. In Houston, there are 28 Bronze Market plans out there, and just one HDHP (which is among the Bronze plans).

By the top of 2025, Catastrophic plans can by no means be HDHPs, since their out-of-pocket limits are too excessive they usually cowl as much as three main care visits pre-deductible. However only a few folks enroll in Catastrophic plans, largely as a result of Market premium subsidies can’t be used with Catastrophic plans, and other people age 30 and older can solely enroll in a Catastrophic plan in the event that they acquire a hardship exemption from the Market.

However tens of millions of individuals have Bronze Market plans. Throughout the open enrollment interval for 2025 protection, about 30% of all Market enrollees chosen Bronze plans.

Along with the revised HDHP definition, H.R.1 additionally relaxes the principles round HSAs and direct primary care (DPC) arrangements. Beginning in January 2026, having a DPC membership (along with an HDHP) will not disqualify somebody from contributing to an HSA. As well as, the DPC membership charge will probably be thought-about a certified medical expense, which means it may be paid with pre-tax HSA funds.

Why does HSA entry matter?

Contributions to an HSA are pre-tax, funding features or curiosity earned within the account are additionally not taxed, and HSA withdrawals usually are not taxed so long as the cash is used for a certified medical expense.

As well as, HSA contributions reduce a person’s ACA-specific modified adjusted gross income (MAGI), which may have an effect on whether or not the particular person qualifies for Market subsidies. This will probably be significantly vital for folks to know beginning with the 2026 plan 12 months, as the “subsidy cliff” will return in 2026 until Congress acts to increase the subsidy enhancements which are scheduled to sunset at the end of 2025.

So an individual who’s going through the lack of all subsidies in 2026 may discover that by contributing to an HSA, they’ll convey their MAGI into the subsidy-eligible vary. Market enrollees ought to focus on this problem with a monetary planner or accountant earlier than choosing a plan for 2026. If contributing to an HSA makes monetary sense for them, will probably be vital to pick out an HDHP in the course of the open enrollment interval, maintaining in thoughts that Bronze and Catastrophic plans will probably be thought-about HDHPs as of 2026.

Louise Norris is a person medical insurance dealer who has been writing about medical insurance and well being reform since 2006. She has written a whole lot of opinions and academic items concerning the Reasonably priced Care Act for healthinsurance.org.

[author_name]

{kind=link}

436wxz

m8riyi

0nzmtd

r2ih8b

th76mk