Key Issues to Know

Entire life insurance coverage dividend choices present policyholders with flexibility and flexibility. The 4 unique choices are: receiving dividends in money, utilizing dividends to cut back or pay premiums, buying paid-up additions, and accumulating dividends at curiosity. Every possibility has its personal tax implications and concerns, reminiscent of potential taxable revenue, influence on price foundation, and premium cost necessities. Much less widespread choices, reminiscent of long-term care advantages and index credit score choices, present further flexibility and potential for enhanced options.

- Dividend Choices: 4 unique choices: Paid in Money, Scale back/Pay Premium, Buy Paid-up Additions, Accumulate at Curiosity.

- Dividend Possibility Availability: Virtually each life insurer issuing dividend-paying complete life insurance coverage contains the 4 unique choices.

- Dividend Tax Implication: Every dividend possibility carries totally different tax implications.

- Dividend Fluctuation: Dividend funds can range from 12 months to 12 months and this might change how policyholders can use varied dividend choices.

- Progressive Dividend Choices: Life insurers are growing new dividend choices, reminiscent of long-term care advantages, to boost policyholder worth.

Entire life insurance coverage dividend choices are one of many methods a whole life policy provides the policyholder robust versatility. Understanding these totally different choices is essential for the right use of a dividend-paying complete life coverage.

The evolution of dividend choices led to by insurance coverage firm creativity creates much more flexibility and flexibility of complete life insurance coverage. At this time I am going to element the 4 choices discovered with nearly each dividend-paying complete life coverage obtainable. I am going to additionally spend a while detailing some extra distinctive dividend choices obtainable at just some insurers.

The 4 Unique Entire Life Insurance coverage Dividend Choices

The unique 4 choices policyholders have for a complete life dividend are:

These 4 complete life insurance coverage dividend choices didn’t originate at the very same time, however their existence as choices spans an especially very long time. Virtually ever life insurer issuing dividend-paying whole life insurance right this moment contains these 4 choices.

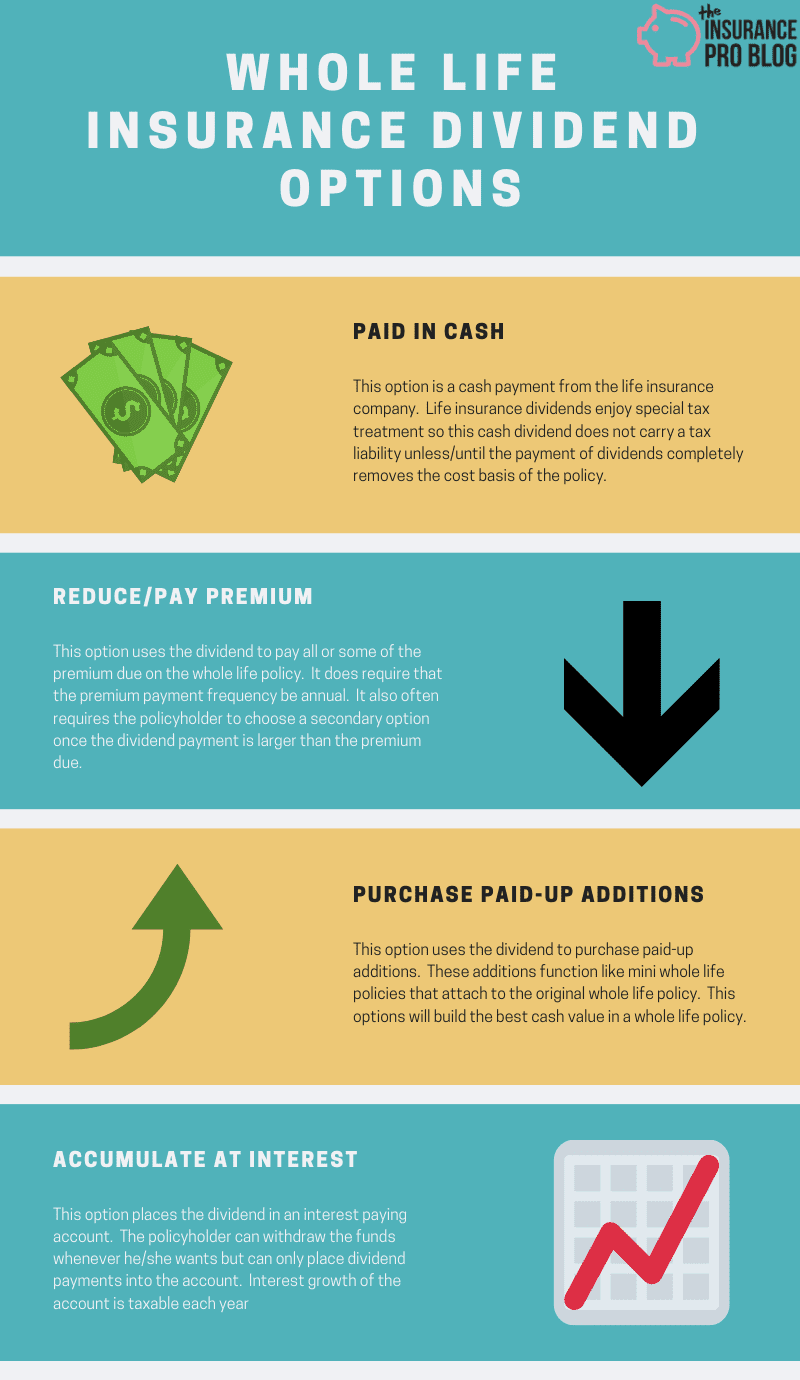

Dividend Possibility: Paid in Money

The choice to obtain the dividend in money is fairly self-explanatory. Every year the life insurer pays the policyholder the dividend within the type of a test. The cost comes on to the policyholder who can then use the money for no matter goal she or he sees match.

U.S. Tax Code classifies the dividend cost on taking part life insurance coverage insurance policies as a refund of premiums paid, so taking the dividend in money doesn’t normally trigger a right away taxable consequence to the policyholder. That is the case as a result of the dividend paid in money is solely lowering the tax foundation established by the policyholder’s cost of premiums.

Ultimately, nevertheless, choosing dividends paid as money might take away the associated fee foundation of the entire life coverage. If this takes place, all dividends paid transferring ahead will carry revenue tax penalties to the policyholder.

An instance will assist make clear this idea.

Sarah owns a ten Pay complete life coverage with a price foundation of $50,000 after 10 years. She opted for the paid in money complete life insurance coverage dividend possibility. As soon as the insurer pays Sarah an combination $50,000 in dividends, Sarah might want to report all future dividends as taxable revenue.

Additionally, notice that if dividend funds do take away the associated fee foundation any withdrawals from the coverage will trigger a tax legal responsibility as properly. Coverage loans proceed to get pleasure from tax-free standing as long as the coverage doesn’t violate the Modified Endowment Contract guidelines.

Dividend Possibility: Scale back/Pay Premium

Selecting to cut back or pay the premium with the dividend means the policyholder chooses to pay a component or all the premium due with the dividend. If the dividend cost is lower than the full premium due, the policyholder might want to pay the remainder of the premium both with cash out of pocket or with money values from the entire life coverage. It is rather more widespread for the policyholder to pay with out-of-pocket cash.

As soon as the dividend cost equals or exceeds the premium due quantity, the dividend pays your complete premium due and the policyholder doesn’t must make any cost to the coverage with any out-of-pocket cash. It is pretty widespread to see older complete life insurance policies utilizing this selection because the policyholder can hold his/her demise profit in power with out having to pay the premium on the life insurance coverage coverage.

Selecting this selection does include some penalties all policyholders ought to perceive.

First, the insurance coverage firm would require the policyholder to vary the cost frequency to annual if it is not paid yearly already. That is essential for policyholders who pay premiums underneath another frequency because it might trigger a money circulation downside. An instance will assist spotlight this level.

Think about that Claire owns a complete life coverage with a $1,000 per 30 days premium she pays. She decides that she needs to make use of the dividend possibility to cut back premium. Within the 12 months she makes this choice the annual dividend on her complete life coverage is $3,000. The annual premium for her coverage is $11,765. Selecting the cut back premium possibility means Claire should change her cost frequency to annual. Her dividend will cut back the premium as a consequence of $8,765, which is due in a single lump sum. If Claire doesn’t have the $8,765 to pay the premium abruptly, the cut back premium dividend possibility shouldn’t be a good suggestion for her.

Although the dividend cost is a refund of premium, utilizing the dividend to pay ongoing premiums due creates an offset that leaves the tax foundation static in all years a policyholder makes use of this selection. This implies the associated fee foundation will neither go up nor go down whereas utilizing the dividend choice to pay premiums.

If the dividend is smaller than the annual premium, any cost made with out-of-pocket cash will enhance the associated fee foundation of the coverage.

It is also price noting that dividend funds can and do fluctuate. So if the dividend cost covers your total premium this 12 months, it may not subsequent 12 months. I deliver this up as a result of life insurance coverage ledgers assume a consistently rising dividend because of the assumption that the dividend scale stays static. This isn’t how most complete life insurance policies work in actual life. Dividends do are likely to develop considerably over time, however that development shouldn’t be at all times linear.

Lastly, know that this dividend possibility is considerably distinctive given that there’s a restrict to the quantity of dividend utilized to this selection. As soon as the dividend is bigger than the premium due on the coverage, the surplus quantity should go someplace. For instance, if in case you have a $10,000 annual premium and the dividend for the 12 months is $12,000, you have got a remaining $2,000 that can’t go in the direction of paying the premium. On this case, the policyholder should select a secondary dividend possibility. Merely, she or he will select one of many different remaining dividend choices and the $2,000 will go in the direction of that possibility.

Dividend Possibility: Buy Paid-up Additions

The dividend choice to buy paid-up additions instructs the insurance coverage firm to take the annual dividend and buy paid-up additions with it. Paid-up additions are mini complete life insurance coverage insurance policies that connect to a fundamental complete life coverage. They earn dividends themselves and have quick money worth.

This dividend possibility will guarantee probably the most bang for the buck by way of premiums producing money give up worth. Put one other means, should you search to maximise the money worth construct up of your complete life coverage, then the choice to buy paid-up additions is the dividend possibility you search.

This dividend possibility can also be how complete life insurance policies accumulate non-guaranteed money worth. The non-guaranteed money worth of an entire life coverage is solely the money worth created by paid-up additions. This “non-guaranteed” money worth is the one money worth that the policyholder can withdraw from a complete life coverage.

Dividend Possibility: Accumulate at Curiosity

The dividend choice to accumulate at curiosity means the insurance coverage firm locations the dividend cost in an interesting-bearing account and provides an curiosity cost to the account every year. The insurer units the rate of interest on these accounts yearly and normally, publicizes it with different data relating to rates of interest reminiscent of mortgage charges, common life rates of interest, and annuity charges. When you have bother finding these bulletins, a fast name to the insurance coverage firm can reply what the present price is.

The speed can change yearly, however all insurers set up a minimal assured price on these accounts.

The policyholder can’t select to put further funds into the curiosity account. So for instance, if a policyholder observed that the rate of interest paid on the account for the accumulate at curiosity possibility was far larger than his/her financial savings account, he/she wouldn’t have the choice to maneuver cash from the financial savings account to the curiosity account on the insurance coverage firm. Solely dividend funds can go to the account.

The policyholder is free to withdraw funds from the curiosity account every time he/she sees match. However is not going to have the choice to place the cash again into the account at a later date. As soon as eliminated, the one solution to construct the account again up is thru future dividend funds on the entire life coverage.

You need to perceive that the curiosity account shouldn’t be a part of the life insurance coverage coverage and doesn’t profit from the tax-friendly therapy related to money worth life insurance coverage.

Curiosity earned underneath this dividend possibility incurs an revenue tax legal responsibility similar to curiosity earned on every other money equal account held at a financial institution or thrift establishment. The policyholder will obtain a 1099-INT on the finish of the 12 months reporting all curiosity paid and should file this along with his/her taxes.

The life insurer is not going to subject a coverage mortgage towards the curiosity account. The values gathered can solely be withdrawn.

At one level within the 1980’s the rate of interest on these accounts grew quicker than dividend rates of interest and a few folks started utilizing this selection extra to maximise curiosity earnings in particular years. Whereas it is at all times attainable we might return to the same state of affairs, this selection normally lags the choice to buy paid-up additions by way of general return on premiums paid to a complete life coverage, particularly given the tax effectivity of money values held inside a complete life coverage by bought paid-up additions.

The Fifth Dividend Possibility

As insurers evolve and turn into extra inventive with product design, a “fifth” dividend possibility appeared that’s fairly widespread–although not as common because the 4 choices talked about above.

This life insurance coverage dividend possibility permits the policyholder to make use of the dividend to buy term life insurance. This selection is often probably the most environment friendly solution to construct demise profit with a complete life coverage–at the least within the brief time period.

The precise execution of this selection varies from firm to firm. The kind of time period life insurance coverage bought shouldn’t be common throughout firms. The quantity of time period life insurance coverage a greenback buys can range from firm to firm and will certainly change because the insured ages.

Much less Frequent Life Insurance coverage Dividend Choices: The New Frontier

Whereas it may not at all times seem this fashion, the life insurance coverage business typically works onerous to innovate and convey new options and advantages to policyholders. In recent times, life insurers developed further options for complete life dividends in an try to boost policyholder worth. These choices are in no way common and sometimes unique or distinctive to only one or a couple of life insurers.

Lengthy Time period Care Advantages

Maybe one of the crucial wanted profit possibility, this dividend possibility builds a pool of cash obtainable for long-term care wants. The insured should qualify to be used of the profit equally to the way in which one would qualify for long-term care insurance coverage (i.e. shedding actions of each day residing or changing into severely cognitively impaired).

Basically, this selection makes use of all or a portion of the dividend to pay for a long run care insurance coverage coverage that’s connected to the entire life insurance coverage coverage. This reduces among the excessive price of long run care insurance coverage premiums discovered on normal stand-alone insurance policies however does normally sacrifice among the profit richness discovered on extra conventional long run care insurance coverage merchandise.

Index Credit score Possibility

This selection seeks to include the advantages of indexing largely present in sure common life insurance coverage insurance policies into a complete life coverage. It causes a change to the traditional dividends payable to the policyholder if they’re prepared to just accept some or all the dividend price be topic to the success or failure of a market index over a sure interval (usually one 12 months). This might significantly improve the payable dividend. Nevertheless it might additionally lead to a considerably decreased dividend cost in any given 12 months if the underlying market index performs poorly.

{kind=link}