Podcast: Play in new window | Download

Within the quest for monetary stability, a de-risked portfolio is the cornerstone of a safe future.

Whole life insurance is an often-overlooked instrument that performs a pivotal position in attaining this stability. By transferring belongings into a complete life insurance coverage coverage with accumulated cash value, you possibly can remodel your retirement financial savings right into a resilient security internet. Not solely does it present life protection, but it surely additionally affords a non-correlated asset that may develop over time and help in mitigating market dangers.

Using a complete life insurance coverage coverage to complement retirement income entails strategic use of policy loans, which may be advantageous as a result of coverage’s gathered money worth.

For those who elect to generate revenue through coverage loans, understanding the implications of paying annual mortgage curiosity is paramount.

Whereas the concept of taking up a mortgage in retirement might sound counterintuitive, the annual revenue potential from the coverage, optimized by savvy dealing with of mortgage curiosity, can considerably exceed the curiosity funds, making a useful monetary state of affairs.

Key Takeaways

-

- A complete life insurance coverage coverage serves as a dual-benefit monetary software, offering each safety and development.

- Coverage loans from entire life insurance coverage can amplify retirement revenue as a result of optimistic arbitrage between revenue and mortgage curiosity.

- Strategic administration of an entire life coverage and its loans maximizes monetary success throughout retirement.

Life Insurance coverage as a Stability Anchor

Within the panorama of financial safety nets, life insurance coverage stands as a stalwart hedge in opposition to market turbulence. Let’s look at how incorporating it into your grand funding scheme enhances stability.

-

-

- Assured Safety: Conventional life insurance coverage merchandise like Entire Life and Listed Common provide a steadfast promise of low to zero volatility, securing your funds in opposition to market fluctuations.

- Money Worth Accumulation: As your coverage matures, it builds a notable money worth, presenting you with a goldmine of economic alternatives on your retirement revenue.

- Mortgage Curiosity Methods: Think about borrowing in opposition to your coverage’s money worth; the curiosity you pay may be considerably outweighed by the annual retirement revenue surge, bestowing you with a profitable arbitrage situation.

-

Take into account dividends—these incremental payouts can contribute to dividend development over time, bolstering your coverage’s money worth. Constantly rising dividends result in heightened yields, aiding in protecting your dwelling bills by a secure, bolstered revenue stream.

Bear in mind, life insurance coverage isn’t a spur-of-the-moment swap however a strategic transfer for sustained prosperity. By leveraging these insurance policies adeptly, you place your self to reap amplified monetary advantages far into the long run.

Stabilizing Your Monetary Future with Life Insurance coverage Asset Switch

Stabilizing your funds in opposition to market fluctuations generally is a prime precedence when approaching retirement. By reallocating a portion of your belongings into a complete life insurance coverage coverage, you could possibly probably safe a extra predictable source of income on your golden years.

Think about you are a 50-year-old who diligently amassed a notable asset base in preparation for retirement. Regardless of this, the potential of market downturns affecting the worth of your portfolio is a sound concern.

One tactic for safeguarding your financial future is to switch $500,000 of your belongings into a complete life insurance coverage coverage which is structured to maximise cash value growth over a dying profit. This switch acts as a buffer by offering an asset that doesn’t undergo from market volatility, guaranteeing the money worth of your coverage is not going to depreciate.

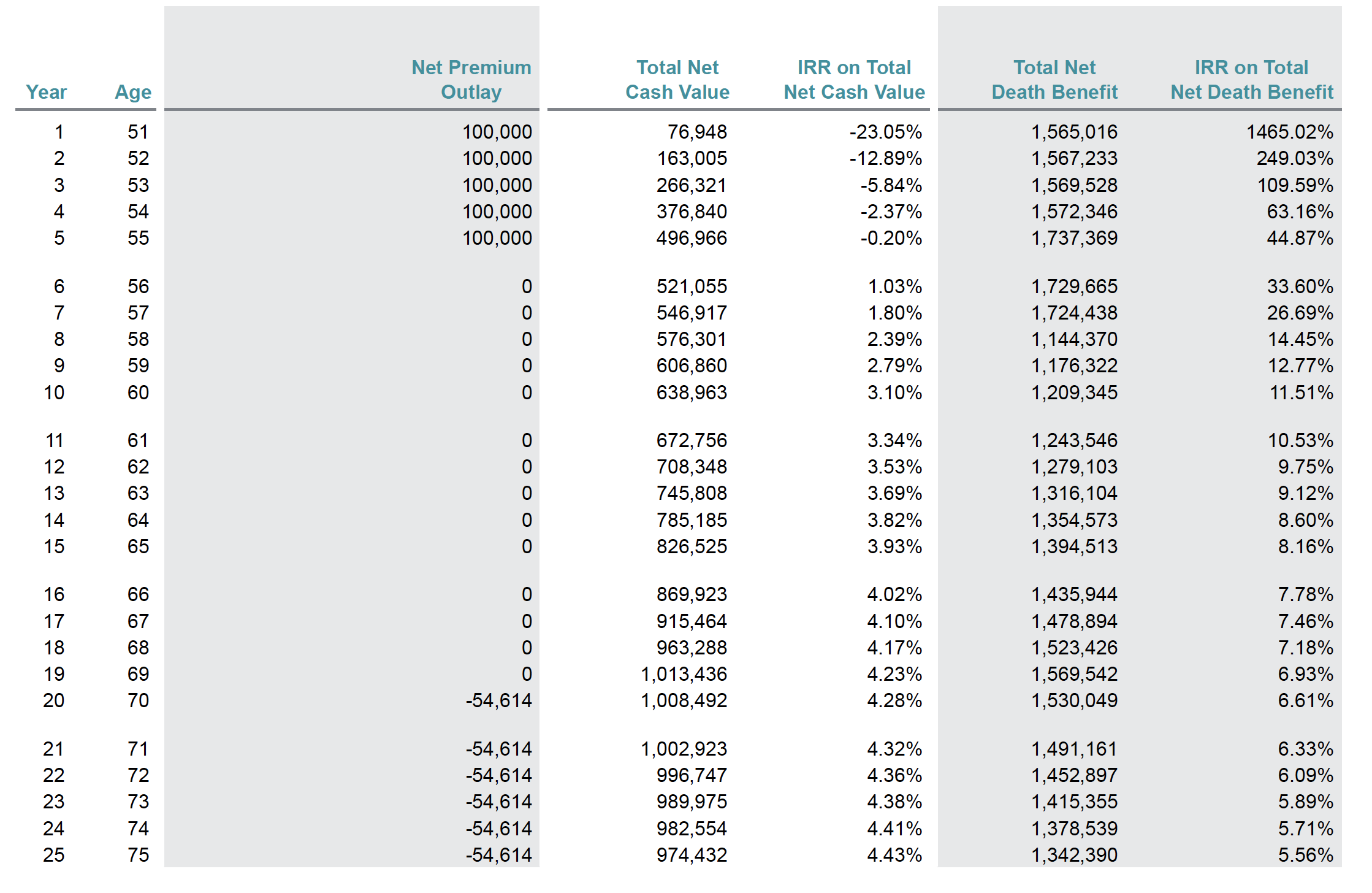

| Years | Money Worth Progress | Revenue Potential |

|---|---|---|

| 10 | 3.10% Return | Substantial Enhance |

| 20 | 4.28% Return | A lot Greater than 4% |

The above desk showcases the enticing returns one would possibly count on over time with such a method. After 20 years, producing revenue near a 5.5% annual distribution price from this coverage’s stability is possible—utterly tax-free and with no compelled withdrawal schedule.

This lack of damaging returns markedly enhances your withdrawal capability in comparison with the everyday 4% secure withdrawal price typically related to retirement planning. Whereas the speed of accumulation might fluctuate, the absence of draw back danger with the coverage amplifies your means to maintain larger withdrawal charges.

For those who decide to make the most of coverage loans for revenue, maintaining with the mortgage curiosity might meaningfully enhance the annual revenue you extract from the coverage. The arbitrage between the upper withdrawal price and the mortgage curiosity might enhance your disposable revenue, proving useful throughout retirement.

In the meantime, assuming they’re invested in an equity-heavy portfolio, your remaining belongings proceed to hold the potential for traditional inventory market development charges, offering a balanced mixture of development and stability on your total asset allocation. This technique is not inflexible; it scales together with your asset base, whether or not you might have extra to allocate or much less.

Making ready Your Portfolio for Future Monetary Stability

Take into account that you just’re 40 and considering the dangers that will come up as you edge nearer to retirement. Your financial savings are substantial, and also you surprise if fine-tuning your technique might proactively mitigate future dangers.

You favor to maintain your belongings invested available in the market to capitalize on potential development over the subsequent few a long time.

Think about channeling $50,000 out of your annual financial savings into a complete life insurance coverage coverage. Historically, you would possibly count on a sure final result from such a method, projected to offer a solid retirement income.

Nevertheless, enhancing this by coordinating together with your different belongings may be much more useful.

Entire life insurance coverage insurance policies assume constant dividends and are sometimes coupled with the idea of taking a loan for income requirements, projected till a set age, like 100.

Sometimes, the mortgage accumulates curiosity, which is not paid out-of-pocket however added to the mortgage stability.

Alternatively, you would possibly think about paying that mortgage curiosity your self utilizing funds from different belongings.

Doing so permits you to trade a portion of your comparatively riskier belongings for an curiosity compensation into your entire life insurance coverage coverage. This transfer might probably skyrocket your annual revenue as a result of coverage, producing secure, non-taxable income.

Let’s break it down:

| Years | Mortgage Curiosity Paid | Revenue Gained |

|---|---|---|

| 1-5 | $79,246 | $459,115 |

This trade displays a big revenue enhance—nearly $92,000 yearly—by offsetting some market dangers by your entire life insurance coverage.

You’d want to make sure that the revenue you forgo by reallocating belongings to cowl the mortgage curiosity meets or exceeds what you’d make in the event that they remained invested elsewhere.

Entire life insurance coverage stands out for its low volatility, providing a strong income generation feature in comparison with extra fluctuating belongings.

And when contemplating life insurance coverage revenue, bear in mind it is already adjusted for taxes and charges.

Even in the event you cease relocating funds to cowl life insurance coverage mortgage pursuits sooner or later, you could possibly nonetheless accumulate extra revenue than projected initially.

Discovering the right stability of asset allocation into life insurance coverage as you age is complicated, but it surely’s not about precision. It is about understanding the alternatives when integrating life insurance coverage into your monetary plan and its profound position in minimizing danger.

Incorporating life insurance coverage into your funding combine can open up many choices, presenting a potent means to lower monetary publicity.

Whereas the subject is in depth, life insurance coverage’s prospects warrant additional exploration on one other event.

{kind=link}