For individuals who purchase their very own medical insurance, premiums rose significantly in 2026 after Congress failed to increase federal subsidy enhancements that expired on the finish of 2025. Tales of customers going through unaffordable medical insurance premiums are widespread. You’re not alone should you really feel like you possibly can’t afford medical insurance.

Why you won’t qualify for Medicaid

We’ll talk about non-public medical insurance in a second, but when well being protection feels unaffordable and also you’re additionally not eligible for Medicaid, you may need questioned why you possibly can’t enroll in Medicaid. There are a couple of causes this is likely to be the case:

- You is likely to be in a state that hasn’t expanded Medicaid below the ACA (extra about that under).

- Your earnings is likely to be above the eligibility minimize off for Medicaid.

- You is likely to be a latest (inside the final 5 years) immigrant.

- Your children is likely to be Medicaid/CHIP-eligible however you won’t be, as a result of the earnings limits are increased for youths.

Now let’s check out a couple of eventualities to elucidate why you is likely to be going through unaffordable medical insurance premiums, and what you may have the ability to do about it.

Situation 1: You earn an excessive amount of to qualify for a subsidy

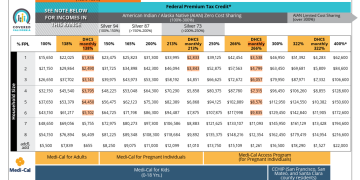

The “subsidy cliff” returned in 2026, as a result of expiration of the federal subsidy enhancements. Which means federal premium subsidies (premium tax credit) are not obtainable to Market enrollees with family earnings above 400% of the federal poverty degree (FPL), no matter how costly their protection choices are. (Observe that state-funded subsidies do lengthen above 400% of FPL in Connecticut, New Jersey, and New Mexico.)

What are you able to do to qualify for subsidies?

Should you misplaced your subsidy altogether on the finish of 2025, it’s possible as a result of your family ACA-specific Modified Adjusted Gross Earnings (MAGI) is over 400% of FPL. (For 2026 protection within the continental United States, meaning you earn greater than $62,600 for a single individual, or greater than $128,600 for a household of 4).

Eligibility for a federal Market premium tax credit score requires {that a} family’s Modified Adjusted Gross Earnings (MAGI) be at or under 400% of the Federal Poverty Degree (FPL). Relying on how far above this threshold your projected earnings is, it could be attainable to carry your MAGI inside the required vary. That is usually finished in certainly one of two methods:

- Adjusting projected earnings in case you are working fewer hours, taking up fewer shoppers, or in any other case incomes much less.

- Reducing MAGI through allowable tax deductions, together with contributions to pre‑tax retirement accounts or well being financial savings accounts.

In case your earnings is simply too excessive to qualify for subsidies, you’ll pay full value for no matter plan you choose. Here are some tips for choosing the plan that best fits your needs and budget.

Should you’re not subsidy-eligible and you like a Silver plan, you may contemplate an off-exchange plan. These are ACA-compliant individual-market insurance policies, however in most states, full-price Silver plans are cheaper off-exchange than on-exchange. It is because the price of cost-sharing reductions is added to the premiums for on-exchange Silver plans in most states.

Premium subsidies usually are not obtainable for off-exchange plans. However should you’re not eligible for subsidies as a result of your earnings, you gained’t be giving up something by choosing an off-exchange plan. (“Off-exchange” refers to totally ACA-compliant individual-market plans, and doesn’t embody non-ACA-compliant plans. These are addressed in additional element under.)

Should you choose a Bronze or Gold plan, the full-price premiums for these plans are usually the identical on-exchange or off-exchange as a result of there are not any CSRs impacting the worth on or off change. However relying on the place you reside, there could also be insurers that provide protection solely on-exchange or solely off-exchange. So should you’re not subsidy-eligible, a complete comparability of each on-exchange and off-exchange plans offers you a full image of what’s obtainable in your space.

(No matter whether or not you’re buying on-exchange or off-exchange, you possibly can full the method your self or do it with assist from a dealer, which gained’t price you something.)

Situation 2: You qualify for subsidies, however protection nonetheless appears unaffordable

You’re definitely not alone should you’re on this class. Most Market enrollees are nonetheless eligible for subsidies in 2026, however after-subsidy premiums had been projected to greater than double in 2026, as a result of expiration of the subsidy enhancements on the finish of 2025.

As famous above, enrollees with family earnings above 400% of FPL misplaced their subsidies altogether on the finish of 2025, leading to substantial premium will increase. However even for individuals who nonetheless qualify for subsidies, the subsidies now cover a smaller share of enrollees’ total premiums. To proceed to have Market protection in 2026, these enrollees should both pay increased premiums, downgrade their protection, or each.

KFF surveyed Market enrollees in November 2025, asking what they might do when confronted with web premiums that had been greater than doubling. Greater than half indicated that they might both choose a plan with decrease premiums however increased deductibles and co-pays, or drop their protection altogether.

In case your protection feels unaffordable even with subsidies, there are a few choices to make it extra inexpensive:

- Cut back MAGI. So long as your MAGI stays above the Medicaid eligibility threshold in your state (and doesn’t drop under 100% of FPL), a decrease MAGI will lead to a bigger subsidy. You possibly can use a subsidy calculator to see how modifications in your MAGI will have an effect on the dimensions of your subsidy.

- Downgrade to a plan with a decrease premium. A number of state-run Marketplaces have revealed information on 2026 plan picks, and there was a clear trend towards higher enrollment in Bronze plans (which have increased out-of-pocket prices however decrease premiums than Silver or Gold plans). However at this level, most present enrollees gained’t have a chance to alter their protection for the remainder of the 12 months, as open enrollment for 2026 has ended and most particular enrollment durations restrict present enrollees to a unique plan on the identical metallic degree as their present plan.

Situation 3: You’re within the protection hole

The protection hole just isn’t new in 2026. It has all the time existed in 9 states that haven’t expanded Medicaid as called for in the ACA: Alabama, Florida, Georgia, Kansas, Mississippi, South Carolina, Tennessee, Texas, and Wyoming. As a result of these states have chosen to not increase Medicaid, many grownup residents with earnings under the federal poverty degree usually are not eligible for any monetary help with their well being protection and usually are not eligible for Medicaid.

Learn more about the coverage gap.

What are you able to do to qualify for monetary help?

Should you’re an grownup in a kind of 9 states and your earnings is under the federal poverty degree, you’re not eligible for Market subsidies. You could discover that you just’re not eligible for Medicaid both (until you’re pregnant or the mother or father of a minor little one, though Medicaid earnings guidelines for this fluctuate by state).

To turn into eligible for Market subsidies, you would wish an ACA-specific modified adjusted gross earnings (MAGI) of no less than 100% of the prior 12 months’s FPL.

For 2026 protection, that’s $15,650 for a single grownup, or $21,150 for a family of two.

Observe: Should you’re in a protection hole state and also you enter an earnings under the FPL on the Marketplace plan comparison tool, it should inform you that you just aren’t subsidy eligible, however it gained’t inform you why. The reason being that your earnings is under the FPL.

Here’s how MAGI is calculated under the ACA. Observe that it’s gross earnings, reasonably than take-home pay, and it is totally different than the MAGI used for different functions.

You should definitely embody all earnings, and keep in mind it’s family earnings, not simply your personal earnings.

Should you’re within the protection hole and your earnings will increase to no less than the FPL, you’ll qualify for a special enrollment period to enroll in a Marketplace plan.

Medicaid eligibility varies by state, with the states that expanded Medicaid eligibility below the Reasonably priced Care Act masking a a lot better portion of the low-income grownup inhabitants. Should you’re affected by the protection hole, you could discover that you just’d truly be eligible for Medicaid should you lived in certainly one of your neighboring states.

Beginning in 2027, Medicaid recipients in growth states will face a work requirement (nationwide), which would require no less than 80 hours per 30 days of labor or different neighborhood engagement.

Situation 4: You can’t afford ACA-compliant medical insurance

Should you’ve tried the entire above methods and may’t make an ACA-compliant well being plan work together with your price range, you will have already dropped your protection or be planning to take action quickly.

There are some extra protection choices you could contemplate, which is likely to be higher than going with none protection in any respect. None of those options is regulated by the ACA. Some aren’t thought of insurance coverage in any respect, and thus aren’t topic to a state’s insurance coverage legal guidelines. As a result of these plans aren’t ACA-compliant, they don’t must cowl the important well being advantages, sometimes exclude pre-existing situations, and usually have annual and lifelong profit caps. However relying in your circumstances and price range, they might pay for some well being care prices that you’d in any other case pay totally out-of-pocket should you had no protection in any respect. It’s vital to evaluate the plan particulars completely earlier than making a call.

Non-ACA-compliant insurance coverage choices

These embody short-term health insurance, fixed–indemnity plans, and numerous varieties of supplemental coverage reminiscent of accident insurance coverage and important sickness insurance coverage. Quick-term medical insurance availability varies by state: In some states there are not any plans obtainable, whereas in others there are plans obtainable with whole durations of as much as three years, together with renewals. None of those plans are thought of complete protection below the ACA.

Non-ACA-compliant choices that aren’t thought of insurance coverage

There are a selection of “protection choices” that aren’t truly insurance coverage, though customers aren’t all the time conscious of that. These embody, for instance, direct primary care memberships, Farm Bureau plans available in certain states, and health care sharing ministry plans.

The particular advantages fluctuate from one plan to a different. However since these kind of protection usually are not thought of insurance coverage, customers who’ve issues with them can’t flip to the state insurance coverage division for help.

Free and low-cost well being care

Relying in your monetary state of affairs, you could qualify totally free or low-cost care at a federally certified well being heart. (Here’s a tool that can help you find one near you.)

Nearly all hospital emergency departments are required to evaluate and stabilize sufferers no matter their potential to pay. However the hospital can nonetheless invoice you for the care you obtain within the emergency division.

get assist discovering protection

There are folks on-line, on the telephone, and in your neighborhood who may help you with the method of getting well being protection. You don’t must pay something for his or her help, as premiums are the identical whether or not you have got help or take a DIY strategy. Right here’s an summary of the assistance that’s obtainable to you:

- Agents and brokers may help with on-exchange or off-exchange plans. They obtain a fee from the insurance coverage provider in the event that they enroll you in a plan, however it would not have an effect on the worth you pay.

- Navigators and Certified Application Counselors (CACs) may help with on-exchange plans in addition to Medicaid

- The Market name heart can reply questions and assist with enrollment. Should you’re in a state that uses HealthCare.gov, the quantity is 1-800-318-2596. Should you’re in a state that runs its personal change (20 states plus DC), there can be a state-run name heart.

- The “find local help” instrument on HealthCare.gov will allow you to see brokers, brokers, Navigators, and CACs in your space. State-run Marketplaces have related instruments.

- An Enhanced Direct Enrollment (EDE) entity can stroll you thru the enrollment course of for an on-exchange or off-exchange plan. See a current list of approved EDE entities.

- Dial 211. Should you aren’t certain the place to show, calling 211 will get you to a neighborhood or regional name heart that may join you to useful well being protection assets.

Louise Norris is a person medical insurance dealer who has been writing about medical insurance and well being reform since 2006. She has written lots of of opinions and academic items concerning the Reasonably priced Care Act for healthinsurance.org.

[author_name]

![[Fuel-Efficient Cars Guide] Hong Kong 10 Driving Tricks to Save Gas + 5 Most Gas-Environment friendly Automobiles](http://marketibiza.com/wp-content/uploads/2026/04/Fuel-saving-car-recommend.webp-120x86.webp)

{kind=link}

Ethereum Mining Made Easy: Step-by-Step Guide https://dropeth.surge.sh

Как выгодно купить iPhone в Тюмени?

[url=https://tmn.applemarketrf.ru/catalog/iphone/iphone-17/]купить iphone тюмень[/url]

Хотите приобрести новый смартфон Apple, но сомневаетесь, где лучше всего совершить покупку в Тюмени? Мы подготовили подробный гид по местам продаж, ценам и специальным предложениям, чтобы вы могли выбрать лучший вариант покупки своего нового iPhone.

Почему стоит купить iPhone в Тюмени

Покупка техники Apple в Тюмени имеет ряд преимуществ:

[url=https://tmn.applemarketrf.ru/catalog/iphone/]купить айфон[/url]

– Официальная гарантия производителя

– Быстрая доставка в пределах города

– Возможность лично ознакомиться с устройством перед покупкой

Кроме того, местные магазины часто предлагают акции и скидки, благодаря которым покупка становится ещё выгоднее.

[url=https://tmn.applemarketrf.ru/catalog/iphone/iphone-17-pro/]iphone 17 pro 512 купить тюмень[/url]

Какие модели доступны в продаже?

Сегодня в магазинах Тюмени представлены следующие актуальные модели:

– iPhone 17: новейшая версия смартфона с улучшенной камерой и производительностью

– iPhone 16: отличная альтернатива предыдущему поколению с поддержкой последних технологий

– [url=https://tmn.applemarketrf.ru]айфон 17 купить в тюмени[/url]

– Другие модели предыдущих поколений также остаются популярными среди покупателей

Где можно купить iPhone в Тюмени?

Оффлайн-магазины:

– Торговые центры («Галерея», «Норвежский дом», «Кристалл») — широкий выбор моделей и возможность сразу забрать устройство

– Авторизованные реселлеры Apple — предоставляют гарантию качества и оригинальность продукции

Онлайн-площадки:

– Интернет-магазины («Эльдорадо», «DNS», «Технопарк») — доступные цены и удобные условия доставки

– Авито и Юла — отличный способ сэкономить, покупая б/у устройства

Советы по выбору места покупки

При выборе магазина обратите внимание на следующие моменты:

– Репутация продавца

– Наличие официальной гарантии

– Цена товара и наличие акций/скидок

Используя наши рекомендации, вы сможете легко и быстро купить iPhone в Тюмени, выбрав именно тот магазин, который предложит лучшие условия для вас!

купить айфон 17 512 в тюмени

https://tmn.applemarketrf.ru

A concise and well-centered remark that strengthens the discussion.

Где выгодно купить Айфон в Уфе?

Хотите приобрести новый смартфон Apple, но сомневаетесь, где лучше всего купить iPhone в Уфе? Мы подготовили для вас полезную инструкцию, которая поможет выбрать надежный магазин и совершить выгодную покупку.

[url=https://applemarketrf.ru]iphone 17 купить уфа [/url]

Почему стоит купить Айфон в Уфе

Смартфоны Apple известны своим качеством сборки, надежностью и длительным сроком службы. Однако многие покупатели сталкиваются с проблемой выбора надежного продавца. Рассмотрим, почему именно Уфа является хорошим местом для покупки iPhone.

Преимущества покупки в Уфе

[url=https://applemarketrf.ru]купить айфон[/url]

– Широкий выбор моделей и цветов.

– Возможность личного осмотра товара перед покупкой.

– Наличие официальных сервисных центров для гарантийного обслуживания.

– Доступ к местным акциям и скидкам.

Как правильно купить iPhone в Уфе

[url=https://applemarketrf.ru]айфон 17 256 гб уфа купить [/url]

Чтобы избежать неприятных сюрпризов, следуйте нашим рекомендациям:

1. Выберите проверенный магазин. Лучше всего покупать смартфоны в крупных сетевых магазинах электроники или специализированных точках продаж Apple.

2. Проверьте гарантию. Обязательно убедитесь, что устройство имеет официальную российскую гарантию.

3. Осмотрите товар. Проверьте внешний вид смартфона, наличие повреждений и работоспособность всех функций.

4. Сравните цены. Изучите предложения разных магазинов, чтобы выбрать наиболее выгодное предложение.

[url=https://applemarketrf.ru/catalog/iphone/iphone-17-pro/]iphone 17 pro купить в уфе[/url]

Рекомендации по выбору модели

Перед тем как купить iPhone, определитесь с моделью, которая соответствует вашим потребностям. Вот некоторые рекомендации:

– Если вам нужен компактный и недорогой вариант, обратите внимание на iPhone SE.

– Для любителей больших экранов подойдет iPhone 13 Pro Max.

– Хотите максимальную производительность и автономность? Тогда ваш выбор — iPhone 14 Pro.

Заключение

Теперь вы знаете, как правильно купить iPhone в Уфе. Следуя нашим советам, вы сможете сделать осознанный выбор и стать счастливым обладателем качественного устройства.

iphone 17 pro купить в уфе

https://applemarketrf.ru

Сначала короткий осмотр и проверка совместимостей, затем — инфузионная терапия с мониторингом давления/пульса/сатурации, после — инструктаж семьи и назначение контрольного контакта. Такой порядок снижает тревогу и делает ночь предсказуемой: понятно, чего ждать, когда отдыхать и в какой момент связываться с врачом.

Подробнее можно узнать тут – [url=https://vyvod-iz-zapoya-sergiev-posad8.ru/]narkologicheskaya-klinika-vyvod-iz-zapoya[/url]