At the very least 5 well being insurers have introduced plans to go away the ACA Market after 2026, affecting greater than 600,000 enrollees throughout a number of states. The exits are elevating new questions concerning the stability of the person market and whether or not further insurers might comply with.

Though insurer participation within the ACA Market has fluctuated for years, the most recent withdrawals come at a time of rising uncertainty pushed by increased premiums, declining enrollment, and federal rule modifications that would additional reshape the market in 2027.

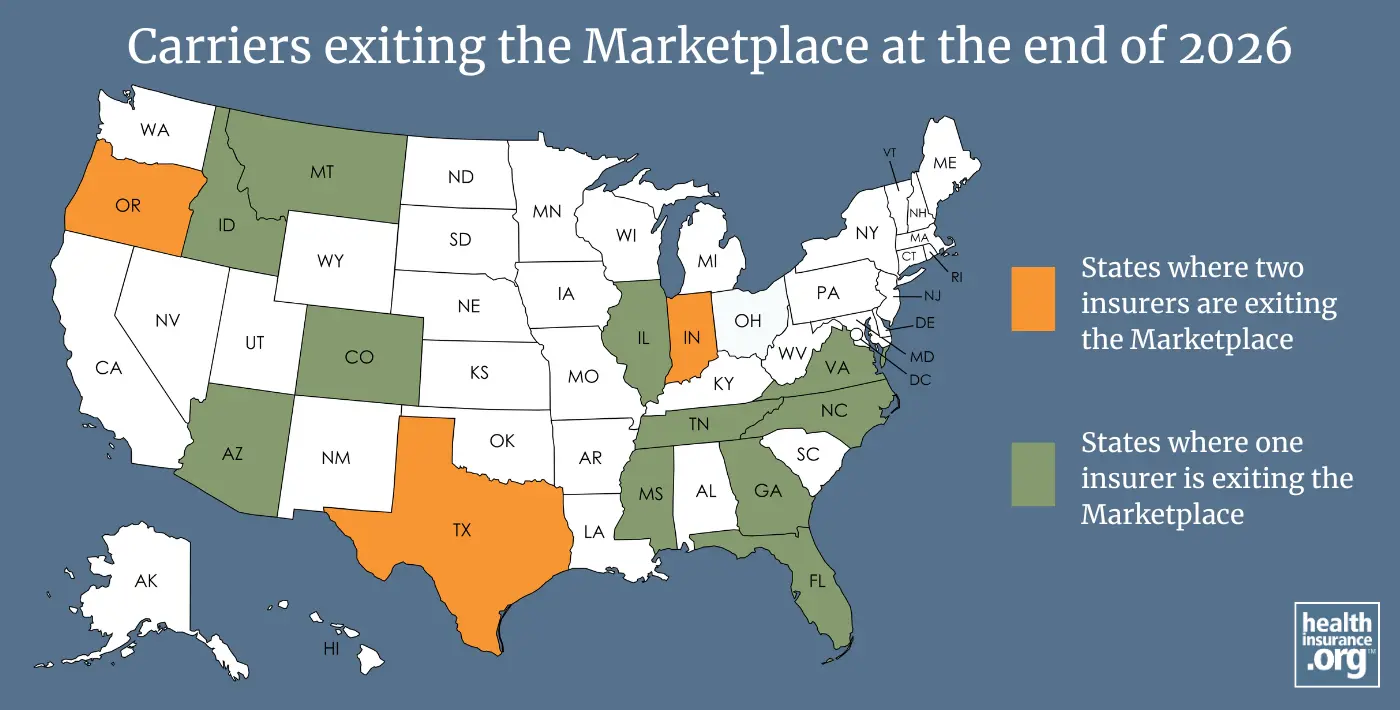

Which carriers have introduced they’re leaving the Market?

Up to now, a minimum of 5 insurers have introduced that they may now not provide Market plans after the top of 2026. They embrace:

- Cigna, which gives Market plans in Arizona, Colorado, Florida, Georgia, Illinois, Indiana, Mississippi, North Carolina, Tennessee, Texas, and Virginia. Throughout these 11 states, Cigna at the moment covers about 369,000 Market enrollees. Cigna won’t provide Market protection in any state in 2027.

- Baylor Scott & White Well being Plan, which covers about 100,000 Market enrollees in Texas.

- CareSource will now not provide Market protection in Indiana, the place it at the moment insures about 60,000 folks. CareSource gives Market plans in 9 states in 2026, and it’s unclear whether or not some other states the place CareSource gives plans can be affected.

- PacificSource will now not provide Market protection in Idaho, Montana, or Oregon, the place a mixed 60,000 folks have PacificSource Market plans.

- Windfall Well being Plan will now not provide Market plans in Oregon. On the finish of 2025, there have been practically 36,000 Oregon Market enrollees with Windfall plans.

Throughout these 5 carriers, greater than 600,000 folks might want to choose new Market plans for 2027.

Might further insurer exits nonetheless be forward? Presumably. But it surely’s nonetheless early within the 2027 fee submitting season, and the total image of Market participation could not develop into clear till a lot nearer to open enrollment, since some insurers have traditionally waited till the autumn to announce Marketplace exits.

Will any carriers exit the market earlier than the top of 2026?

Traditionally, most Market insurer exits have occurred on the finish of the calendar yr. Mid-year shutdowns have been uncommon, with notable exceptions together with some ACA CO-OP failures within the early years of the exchanges and the collapse of Friday Health Plans in 2023.

So far, all the Market exits introduced this yr are scheduled for the top of 2026, so they don’t have an effect on anybody’s 2026 protection. Enrollees can hold their present plan by way of the top of the yr so long as they proceed to pay their month-to-month premiums.

Be taught extra: What should consumers do if their insurer is leaving the Marketplace?

Why are carriers pulling out of the Market?

Business teams and insurers have described the present setting as a “excellent storm” for the person market.

A number of main modifications are contributing to that uncertainty, together with:

All of those elements are inflicting enrollment declines and a much less wholesome threat pool within the particular person market.

Declining Market enrollment drives service selections

Market enrollment declined in 2026, after 5 years of regular progress – and based on a Wakely evaluation, effectuated enrollment is projected to be 17% to 26% decrease in 2026 than it was in 2025.

Though we don’t but have official nationwide 2026 effectuated enrollment knowledge from Facilities for Medicare & Medicaid Companies (CMS), NOTUS (Information of the US) has obtained inner CMS paperwork and reported that 21% of HealthCare.gov enrollees had been disenrolled within the early months of 2026 for failure to pay premiums. Throughout state-run Marketplaces, the drop-off was a lot smaller, at about 8%, due partly to the supplemental subsidies offered by some state-run Marketplaces.

However nationwide, about 17% of the individuals who chosen a plan in the course of the open enrollment interval for 2026 (or whose protection was mechanically renewed) have already misplaced their protection for failure to pay premiums.

And a few state-run Marketplaces are displaying important declines in effectuated enrollment in early 2026. For instance, Georgia’s effectuated Market enrollment dropped from practically 1.5 million in early 2025 to 950,000 by April 2026. In Washington state (which does provide state-funded subsidies), effectuated enrollment as of February 2026 was down greater than 15% from the place it had been a yr earlier.

Total, CMS tasks that common effectuated Market enrollment can be about 18.9 million folks in 2026, though it might doubtlessly drop to as little as 16.5 million. As compared, common effectuated Market enrollment was 22.3 million folks in 2025.

A serious cause for the enrollment decline is the expiration of enhanced federal subsidies on the finish of 2025. Many Market customers saw premiums rise sharply when these subsidy enhancements expired. Though thousands and thousands of individuals switched to plans with higher out-of-pocket costs or dropped their protection altogether, common internet premiums within the Market still rose by 58% in 2026.

That sharp improve in internet premiums is the first cause so many individuals didn’t pay their premiums within the early a part of 2026. That issues as a result of more healthy customers are typically extra more likely to drop protection when premiums improve, whereas folks with ongoing medical wants usually tend to hold their insurance coverage.

As more healthy folks depart the market, insurers are left masking a smaller however much less wholesome threat pool. That will increase common medical prices per enrollee and places upward strain on premiums.

The Trump administration’s rule modifications for 2027 might intensify these pressures even additional. Federal regulators have projected that the brand new guidelines might result in as many as 2 million further folks leaving the Market.

CMS has additionally acknowledged that more healthy enrollees could also be extra more likely to lose or discontinue protection beneath the brand new guidelines, doubtlessly contributing to further premium will increase (though CMS notes that these premium will increase could also be offset by extra eligibility verification for particular enrollment durations and decrease trade consumer charges).

Market participation is finally a enterprise choice

For insurers, participation within the Market is basically a monetary calculation.

Insurers constantly consider whether or not Market protection is worthwhile and whether or not the market seems secure sufficient to justify continued participation. When enrollment declines, threat swimming pools worsen, and coverage uncertainty will increase, some insurers determine the enterprise threat is now not worthwhile.

There will also be state-specific coverage elements concerned. New Mexico, for instance, requires Medicaid managed care insurers to additionally provide statewide Market protection. However in most states, Market participation selections are largely pushed by insurers’ evaluation of profitability and general market stability.

Present withdrawals mirror a well-known cycle

Insurer participation within the Marketplaces has been cyclical over time, typically growing when the person market was more healthy and bigger, and reducing when it was sicker and smaller. We are able to see a transparent illustration of this after we have a look at how Aetna’s Market participation has shifted in response to altering market circumstances.

On the finish of 2016, Aetna exited the Market in 11 of the 15 states the place it provided protection. The corporate then totally exited the ACA exchanges after 2017.

However Aetna later returned to the Market in 2022 and expanded into further states in 2023. Nonetheless, the corporate as soon as once more totally exited the Market after 2025.

That sample mirrors broader Market tendencies over the previous decade.

Insurer participation declined considerably in 2017 and 2018 amid repeated congressional repeal efforts and coverage uncertainty surrounding the ACA.

Participation later rebounded in the course of the Biden administration, when enhanced subsidies and different coverage modifications (together with a low-income special enrollment period, fixing the “family glitch,” and Marketplace access for DACA recipients) made Market protection extra reasonably priced and accessible, leading to much more folks with Market protection.

However the variety of insurers taking part within the Market declined once more for 2026, after a number of of the Biden-era modifications had been eradicated. This was the primary general decline in insurer participation since 2018.

Nonetheless, at present’s Market participation ranges stay considerably stronger than they had been in the course of the market instability of 2017 and 2018.

In 2018, greater than 1 / 4 of Market enrollees solely had entry to plans from a single insurer. In contrast, regardless of the current decline in participation, only one% of HealthCare.gov enrollees in 2026 had entry to only one insurer’s plans.

What ought to customers anticipate subsequent?

Further Market exits stay potential over the approaching months, as insurers finalize 2027 charges participation selections.

However whereas the present insurer withdrawals and declining Market enrollment are important, the person market has confirmed to be resilient. It has gone by way of cycles of enlargement, contraction, coverage modifications, and insurer repositioning over the previous decade.

The approaching months will present a clearer image of whether or not 2027 represents one other short-term contraction – or the start of a extra important shift within the Market panorama.

[author_name]

{kind=link}