Should you’ve checked out your 2026 Market medical health insurance choices and also you’re feeling sticker shock since you’re seeing considerably bigger premiums, don’t panic simply but. Right here’s what it is advisable know as open enrollment for 2026 well being protection will get underway.

Who’s experiencing Market sticker shock?

For the 93% of Market (trade) enrollees who’re receiving premium subsidies (premium tax credit) for 2025 protection, the after-subsidy premium for the benchmark (second-lowest-cost Silver) plan is projected to extend by 114% in 2026, until Congress takes motion to increase the subsidy enhancements which are scheduled to expire at the end of 2025.

For the 7% of Market enrollees who don’t get subsidies – plus anybody who buys ACA-compliant particular person market protection outside the exchange – full-price (unsubsidized) premiums are growing by a median of 26%, though this can fluctuate significantly from one coverage to a different.

There are greater than 23 million folks with Market protection, and given the typical fee will increase, most of them may very well be experiencing a point of sticker shock after they have a look at their 2026 premiums.

Listed here are 5 steps you may take to raised perceive modifications in Market insurance coverage prices and take motion throughout open enrollment.

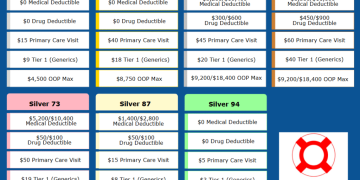

1. Overview the obtainable plans. (These gained’t change.)

Insurers have finalized and acquired regulatory approval for the individual-market plans which are obtainable in every state’s Market for 2026. So though after-subsidy premiums might change if Congress takes motion to increase or modify the subsidy enhancements, the protection particulars of the obtainable plans is not going to change.

Meaning you may take a while now to overview particulars like deductibles, out-of-pocket maximums, lined drug lists, and supplier networks, to get an thought of what your protection choices are for 2026. Your current plan might not be available for 2026, or there might be new plans available in your area, relying on the place you reside. And even in areas the place plans proceed to be supplied by the identical insurers that supplied them in 2025, there may very well be modifications within the protection specifics.

2. Perceive your earnings as a proportion of the federal poverty stage (FPL)

Your eligibility for 2026 Market premium subsidies is predicated on how your projected 2026 family earnings compares to the 2025 federal poverty stage. (Word that these numbers are increased in Alaska and Hawaii.)

Here’s how household income (MAGI) is calculated under the ACA.

Until Congress extends the subsidy enhancements, enrollees will now not be eligible for premium subsidies in 2026 if their 2026 family earnings is greater than 400% of the 2025 FPL. Should you’re within the continental United States, right here’s what 400% of FPL quantities to in annual earnings, for 2026 protection:

- Family of 1: $62,600

- Family of two: $84,600

- Family of three: $106,600

- Family of 4: $128,600

- Family of 5: $150,600

- Family of six: $172,600

For this reason – until Congress extends the subsidy enhancements – you’ll see no subsidy in any respect within the Market in case your projected family earnings is above these quantities. (Should you’re in Massachusetts, New Jersey, or New Mexico, you should still see some subsidies, as these states have state-funded subsidies that stretch to enrollees with incomes above 400% of FPL.)

3. Perceive how HSA contributions can have an effect on your MAGI

Contemplate a 60-year-old residing in Atlanta, incomes $63,000. (Here’s how ACA-specific modified adjusted gross income, or MAGI, is calculated.) At that earnings stage, they’re just a bit above 400% of FPL, which suggests they gained’t qualify for any subsidy in any respect in 2026 if Congress doesn’t lengthen the subsidy enhancements. In that case, the lowest-cost plan obtainable to this individual will price $1,079/month in premiums in 2026, which quantities to greater than 20% of their family earnings.

However that lowest-cost choice is a Bronze plan, and all Bronze Market plans will allow enrollees to contribute to a health savings account (HSA) in 2026. So if this individual enrolls in that Bronze plan, opens an HSA, and contributes simply $1,000 to the HSA in 2026, that would bring their household income down to $62,000, which is just a bit underneath 400% of FPL.

That might enable them to keep away from the “subsidy cliff,” and would make them eligible for a major subsidy. Their after-subsidy premium for that lowest-cost plan will drop to only $262/month – just because they enrolled in an HSA-eligible plan, opted to contribute $1,000 to an HSA, and thus lowered their MAGI by $1,000.

That $1,000 HSA contribution (which remains to be their very own cash, and obtainable at any time to pay for medical bills on a pre-tax foundation) ends in them qualifying for a subsidy of $817/month, which covers nearly all of the price of their protection.

This is only one instance, and the specifics will fluctuate relying on the place you reside, how previous you might be, how a lot you earn, and the way a lot you’re in a position to contribute to an HSA. The utmost allowable HSA contribution for 2026 is $4,400 when you’ve got self-only protection, and $8,750 in case your HSA-eligible well being plan additionally covers at the least one extra member of the family.

We suggest that you just communicate with a tax advisor in case you’re contemplating this technique, as there are tax ramifications once you make changes to your earnings. You need to be conscious of all of them earlier than making any monetary choices.

4. Replace your Market account

Now is an effective time to ensure your Market account is updated. If there have been any modifications in your family or your earnings for the reason that final time you up to date your Market account, make sure you report these modifications to the Market.

It’s significantly necessary to undertaking your earnings as precisely as attainable for 2026, and maintain the Market up to date in case you understand mid-year that your earnings projection wasn’t appropriate. It is because 2026 would be the first 12 months when there’s no cap on how much excess advance premium tax credit (APTC) has to be repaid to the IRS.

Should you underestimate your earnings after which find yourself incomes greater than you projected, there will probably be no restrict on how a lot extra APTC you must repay to the IRS once you file your taxes in early 2027.

5. Bear in mind the Dec. 15 deadline (in most states) and keep tuned for updates

You will have till at the least December 15 (or later in some states) to choose a Market plan that may take impact on January 1, 2026. So in case you’re experiencing sticker shock once you see the costs which are at the moment displayed for 2026 protection, you’ve got a few choices:

You possibly can choose a plan now, primarily based on the costs that mirror the expiration of the subsidy enhancements.

Should you do that, keep tuned for updates in regards to the subsidy enhancements. If Congress later extends the subsidy enhancements or extends a modified model of them throughout open enrollment, you’ll have the choice to choose a unique plan if that’s your desire. The final plan you choose will take impact January 1, so long as you make the plan choice by December 15 (or the deadline in your state).

You possibly can maintain off on choosing a plan for now, and keep tuned for updates concerning the federal subsidy enhancements.

Should you determine to delay enrollment within the hopes that the subsidy enhancements will probably be prolonged by Congress, make sure you set a calendar reminder to enroll in a plan earlier than December 15. Should you don’t, your present Market protection will probably be auto-renewed. (Should you’re at the moment uninsured, you’ll proceed to be uninsured in January.) However actively selecting your own plan is generally a better option than relying on auto-renewal.

Louise Norris is a person medical health insurance dealer who has been writing about medical health insurance and well being reform since 2006. She has written tons of of opinions and academic items in regards to the Inexpensive Care Act for healthinsurance.org.

[author_name]

![[Complete Guide to Guangdong Vehicles Traveling South to Hong Kong] Utility course of for entry and non-entry to Hong Kong, driver {qualifications}, car inspection, required paperwork and insurance coverage info](http://marketibiza.com/wp-content/uploads/2025/11/Southbound-Travel-Guide-820x453.webp-120x86.webp)

{kind=link}

This was beautiful Admin. Thank you for your reflections.

I appreciate you sharing this blog post. Thanks Again. Cool.

naturally like your web site however you need to take a look at the spelling on several of your posts. A number of them are rife with spelling problems and I find it very bothersome to tell the truth on the other hand I will surely come again again.

I just like the helpful information you provide in your articles

You’re so awesome! I don’t believe I have read a single thing like that before. So great to find someone with some original thoughts on this topic. Really.. thank you for starting this up. This website is something that is needed on the internet, someone with a little originality!

This is now one of my favorite blog posts on this subject.

Your breakdown of the topic is so well thought out.