Since 2018, federal guidelines have made it doable for shoppers in lots of states to purchase short-term, limited-duration insurance coverage (STLDI) and hold that protection for so long as three years, together with renewals and extensions. (States can set their very own extra stringent guidelines, which is why these guidelines don’t apply nationwide.) However a rule proposed by the Biden administration in July 2023 would considerably restrict the size of STLDI plans.

If finalized, the rule would restrict the preliminary time period of STLDI insurance policies to now not than three months. Although the rule would enable renewal of a coverage, the full length of a plan can be restricted to 4 months, and a purchaser wouldn’t be allowed to buy one other short-term plan from the identical insurer inside 12 months of their preliminary coverage efficient date.

The businesses publishing the rule noted that these adjustments are designed to make sure that short-term protection is used to fill a brief hole between two complete insurance policies, somewhat than serving as a long-term protection answer. The rule can be meant to scale back the quantity of people that inadvertently buy short-term protection when attempting to purchase complete protection.

In introducing the proposed rule, President Biden mentioned his administration is “cracking down” on limited-duration insurance being bought to people who usually don’t perceive the protection after which are stunned once they get hit with giant medical payments.

The proposed change would roll again a 2018 rule that expanded the provision of short-term, limited-duration plans, permitting them to final for as much as three years if the protection is renewable.

In accordance with the Nationwide Affiliation of Insurance coverage Commissioners, 235,775 people were covered under short-term policies as of 2022. Nevertheless, the precise variety of enrollees is unsure as a result of insurance coverage carriers are not required to report enrollment data.

What occurs subsequent?

The Facilities for Medicare & Medicaid Providers is accepting public feedback on the proposed rule till September 11, 2023. Rulemaking is a multi-month course of, so any rule change doubtless gained’t be finalized till late 2023.

If permitted, the foundations wouldn’t apply to new short-term insurance policies till 75 days after the rule is finalized. Insurance policies issued earlier than that date wouldn’t should adjust to the brand new guidelines.

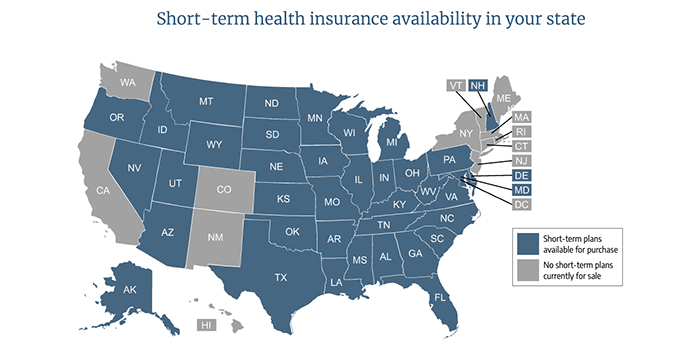

For now, shoppers in lots of states can proceed enrolling in longer-duration short-term plans. We are saying “many states” as a result of though the 2018 rule permits states to permit the sale of longer-duration plans, almost half of the states have adopted stricter limits on STLDI length. (See particulars under for every state.)

Some states have banned the sale of short-term plans outright whereas different states have adopted rules which have brought on insurers to cease promoting the plans.

The Biden administration’s proposed adjustments

The proposed rule published in July 2023, would change all three of the foundations that the Trump administration put in place. These 2018 guidelines:

- Restrict short-term plans to preliminary phrases of as much as 364 days.

- Permit short-term plans to be renewed so long as the full length of the plan doesn’t exceed 36 months.

- Require short-term plan info to incorporate a disclosure to assist folks perceive how short-term plans differ from particular person medical health insurance.

Beneath the Biden administration’s proposed rule:

- New short-term insurance policies can be restricted to preliminary phrases of not more than three months.

- Carriers would be capable of supply renewable insurance policies, however the complete length – together with renewals – couldn’t exceed 4 months. The proposed rule notes that the three-month window is designed to align with the utmost ready interval {that a} new worker could be topic to earlier than being eligible for an employer-sponsored well being plan.

- A shopper wouldn’t be allowed to buy an extra short-term coverage from the identical insurer inside 12 months of the efficient date of the primary coverage.

The required disclosure discover can be up to date to make clear that federal monetary help just isn’t accessible with short-term insurance policies, and that shock steadiness billing protections don’t apply to those insurance policies.

State regulatory flexibility relating to short-term plans

As famous above, HHS made it clear within the 2018 rules that though the federal guidelines expanded the bounds on short-term plan length, states could proceed to implement extra restrictive guidelines, simply as they did previous to 2017. (States can not implement guidelines which are extra lenient than the federal rules.)

States are taking various approaches on short-term plans, with some clearly eager to broaden entry, whereas others want to limit or eradicate short-term plans in an effort to guard their ACA-compliant markets.

In a couple of states – New York, New Jersey, Massachusetts, Rhode Island, and Vermont – short-term plans weren’t bought in any respect as of 2018. And by 2020, 5 extra states – California, Colorado, New Mexico, Maine, and Hawaii – and Washington, DC additionally had no insurers providing short-term plans.

In Washington, the sale of short-term well being plans was discontinued in mid-2022 and no insurers supply short-term well being plans in Washington as of 2023. New Hampshire and Minnesota additionally had no insurers providing short-term well being plans by mid-2023.

As well as, a number of states had already capped the length of short-term plans at three or six months, even earlier than the Obama administration took motion to restrict short-term plans. Different states have subsequently carried out three- or six-month caps on short-term plans.

In the end, there are extra states with their very own restrictions on short-term plans than there are states which are defaulting to the federal guidelines. Use this map to see how states limit short-term plans.

If the Biden administration’s proposed guidelines are finalized, states will now not have the choice to permit short-term insurance policies to have preliminary phrases of greater than three months, or complete durations of greater than 4 months. Insurance policies with longer phrases wouldn’t be thought of short-term plans and must adjust to the ACA’s guidelines for individual-market protection.

Present state limits on length of short-term plans

States permitting short-term plans to have length as much as six months

- Colorado – Six-month preliminary durations are allowed, however insurers stopped providing short-term plans as of 2019.

- Connecticut

- Illinois limits preliminary plan length to 6 months with no renewals.

- Michigan limits preliminary plan durations to 185 days with no renewals.

- Minnesota limits preliminary plan durations 185 days, however no insurers supply plans as of August 2023.

- Nevada limits preliminary plan durations to 185 days with no renewals.

- New Hampshire limits preliminary plan durations to 6 months and 18 months complete inside a two-year interval, however no insurers supply plans as of 2023.

States (and the District of Columbia) permitting short-term plans to have length as much as three months

A handful of states enable short-term plans to have preliminary phrases in step with the brand new federal guidelines (364 days), however place extra restrictive limits on renewals and complete plan length:

- Idaho – “Enhanced” short-term plans are assured renewable for complete length of three years. State limits preliminary length of non-enhanced short-term plans to 6 months with no renewals.

- Kansas – (Just one renewal permitted.)

- Ohio – (Renewals not permitted.)

- South Carolina – (11-month most preliminary time period, and 33-month most length.)

- Wisconsin – (Complete length restricted to 18 months.)

In 14 states and the District of Columbia, no short-term plans can be found for buy. In some instances, state rules ban sale of the plans outright. In others, state rules make it unappealing for insurers to supply short-term plans.

- California – State legislation prohibits the sale of short-term plans.

- Colorado – As famous, plans are technically allowed with six-month preliminary durations, however insurers have stopped providing short-term plans.

- Connecticut

- District of Columbia – Plans are allowed for as much as three months with no renewals, however no insurers supply them.

- Hawaii – As famous, no insurers supply plans below the foundations the state carried out.

- Maine – New guidelines took impact in 2020, and no insurers supply plans.

- Minnesota – No insurers supply plans as of August 2023.

- New Hampshire — No insurers supply plans as of 2023.

- New York

- New Jersey

- Massachusetts – Well being plans are required to be guaranteed-issue, so short-term insurance policies usually are not accessible within the state

- New Mexico – State rules restrict the plans to 3 months and prohibit renewals, however no insurers had been providing plans as of mid-2019.

- Rhode Island – STLDI just isn’t banned, however state guidelines are strict sufficient that no insurers supply these insurance policies

- Vermont – There aren’t any short-term plans accessible in Vermont, however laws was additionally enacted in 2018 to restrict short-term plans to 3 months and prohibit renewals, in case any plans are permitted sooner or later.

- Washington – Plans are allowed for as much as three months, however no insurers supply them.

You need to use the map on this page to see extra particulars about short-term medical health insurance guidelines and availability in every state.

The trail to present short-term federal guidelines

Beneath regulation changes that HHS finalized in 2018 – and in impact since October of 2018 – the preliminary length of short-term plans was lengthened to 364 days with an choice to renew a plan for protection as much as a complete of three years. This 2018 rule reversed regulations – put in place by the Obama administration – that had restricted short-term plan durations to 90 days and didn’t enable renewal of insurance policies.

The 2018 rule additionally established {that a} plan is taken into account “short-term” so long as it has an preliminary time period of lower than a 12 months (not more than 364 days).

However the 2018 rule additionally permits short-term plans to supply enrollees the choice to resume their plans with out extra medical underwriting and use renewal to maintain the identical plan in pressure for as much as 36 months.

Beneath the Trump administration, HHS justified this by noting that the protection has lengthy been referred to as “short-term restricted length” well being protection, and stating that “short-term” and “restricted length” should imply various things, in any other case the phrases can be redundant.

So HHS mentioned that “short-term” refers back to the preliminary time period, which should be below 12 months. However they allowed the “restricted length” half to imply as much as 36 months in complete, below the identical plan.

It’s vital to notice that HHS could have anticipated this to be challenged in court docket, as they included a severability clause for the half about 36-month complete length: If a court docket had been to strike down that provision, the remainder of the rule would stay in place. (A lawsuit was filed over the legality of the brand new short-term insurance coverage rule in September 2018, however that case ended with a ruling in favor of the Trump administration.)

Within the 2018 rule, HHS famous that there’s nothing in federal statute that might stop an individual from enrolling in a brand new short-term plan after the 36 months (or buying an possibility from the preliminary insurer that may enable them to purchase a brand new plan at a later date, with the brand new plan allowed to begin after the complete 36-month length of the prior plan).

So technically, federal guidelines enable folks to string collectively a number of “short-term” plans indefinitely. However as famous above, there are fairly a couple of states with a lot stronger short-term plan rules, and a few states carried out restrictions on short-term plans particularly in response to the brand new federal guidelines.

The disclosure discover required within the 2018 rule was meant to tell shoppers of a number of points of short-term protection: That the plans usually are not required to adjust to the ACA, could not cowl sure medical prices, and will impose annual/lifetime profit limits. The disclosure additionally notes that the termination of a short-term plan doesn’t set off a particular enrollment interval within the particular person market (although it does for group health plans).

Enrollees who develop well being situations whereas coated below a short-term plan – and could also be topic to pre-existing situation exclusions below a brand new short-term plan – would possibly discover themselves with out short-term protection and having to attend till the following open enrollment interval to enroll in Market protection.

Louise Norris is a person medical health insurance dealer who has been writing about medical health insurance and well being reform since 2006. She has written dozens of opinions and academic items concerning the Inexpensive Care Act for healthinsurance.org. Her state well being alternate updates are repeatedly cited by media who cowl well being reform and by different medical health insurance consultants.

[author_name]

{kind=link}